Chengling Gou (2006)

The Simulation of Financial Markets by an Agent-Based Mix-Game Model

Journal of Artificial Societies and Social Simulation

vol. 9, no. 3

< https://www.jasss.org/9/3/6.html >

For information about citing this article, click here

Received: 06-Dec-2005 Accepted: 13-May-2006 Published: 30-Jun-2006

Abstract

Abstract

|

(1) |

|

(2) |

|

(3) |

|

| Figure 1. Three configurations of historical memories |

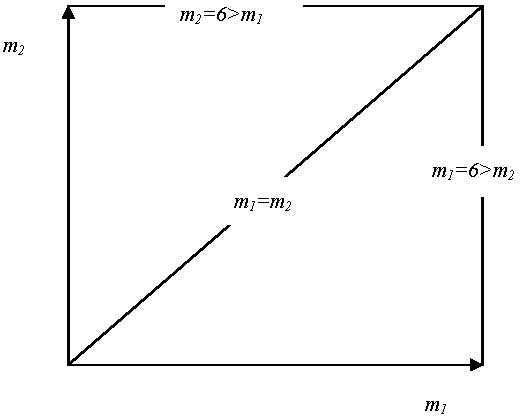

| Table 1: Correlations among R1, R2 and Vol1 when m2=6, and m1 increases from 1 to 6 | |||

| R 1 | R 2 | Vol1 | |

| R 1 | 1 | ||

| R 2 | 0.982 | 1 | |

| Vol1 | 0.985 | 0.996 | 1 |

| Table 2: Correlations among R1, R2 and Vol2 when m1=6, and m2 increases from 1 to 6 | |||

| R1 | R2 | Vol2 | |

| R1 | 1 | ||

| R2 | -0.246 | 1 | |

| Vol2 | 0.148 | -0.892 | 1 |

| Table 3: Correlations among R1, R2 and Vol3 when m1=m2, and they increase from 1 to 6 | |||

| R1 | R2 | Vol3 | |

| R1 | 1 | ||

| R2 | 0.977 | 1 | |

| Vol3 | -0.859 | -0.737 | 1 |

|

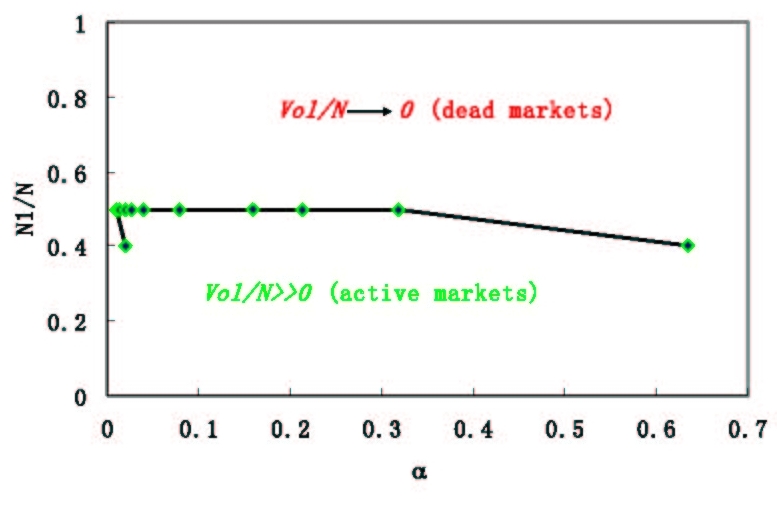

| Figure 2. Two-phase phenomenon of local volatilities under simulation condition of m1 < m2, where α = 2m1 / N |

|

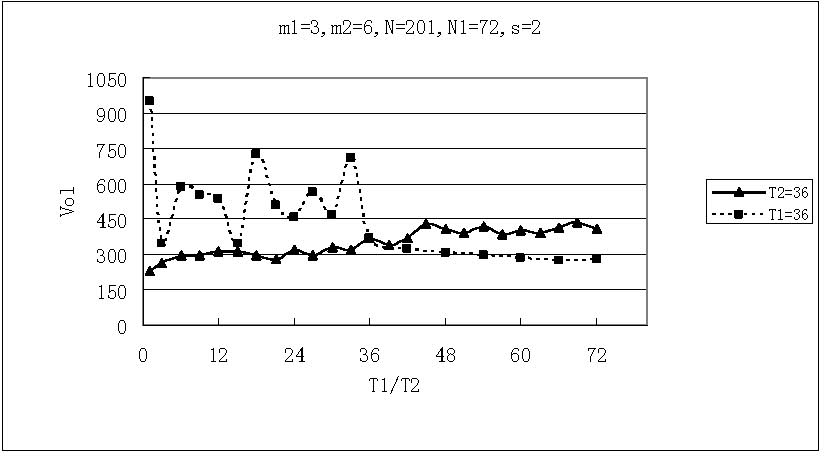

| Figure 3. Relations between means of local volatilities and time horizon T1 (T2) when T2=36 (T1=36), m1=3, m2=6, N=201, N1=72 and s=2 |

|

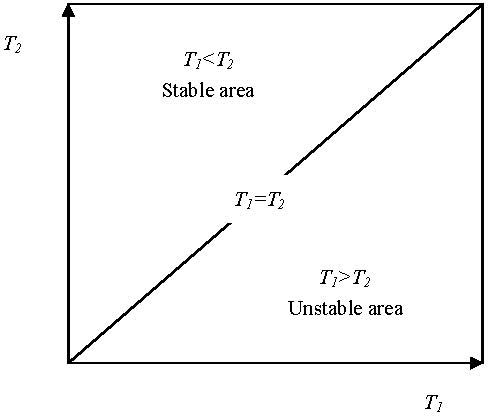

| Figure 4. Two-phase phenomenon of local volatilities in T1-T2 space under simulation condition of m1=3, m2=6, N=201, N1=72 and s=2 |

|

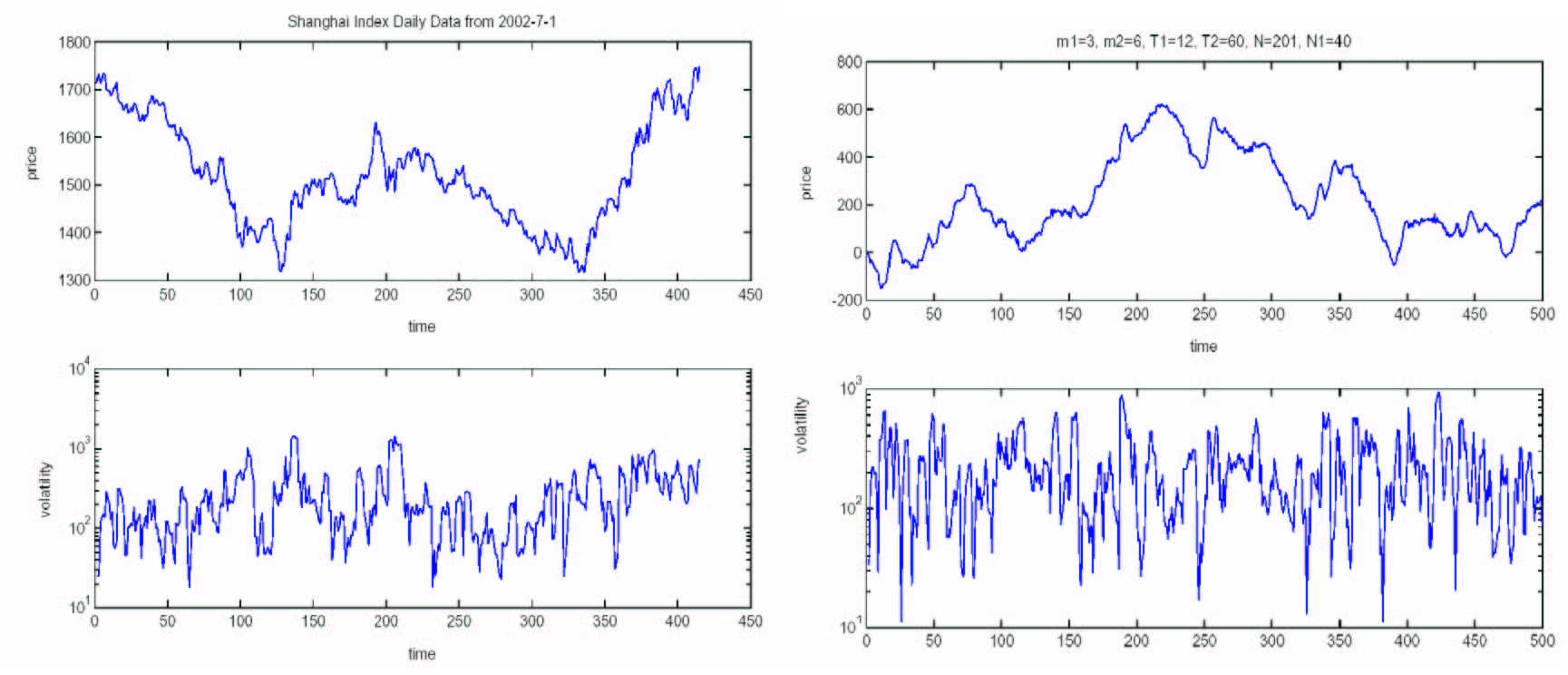

| Figure 5. Time series and local volatilities of Shanghai Index daily data and the mix-game with parameters of m1=3, m2=6, T1=12, T2=60, N=201, N1=40 and s=2 |

|

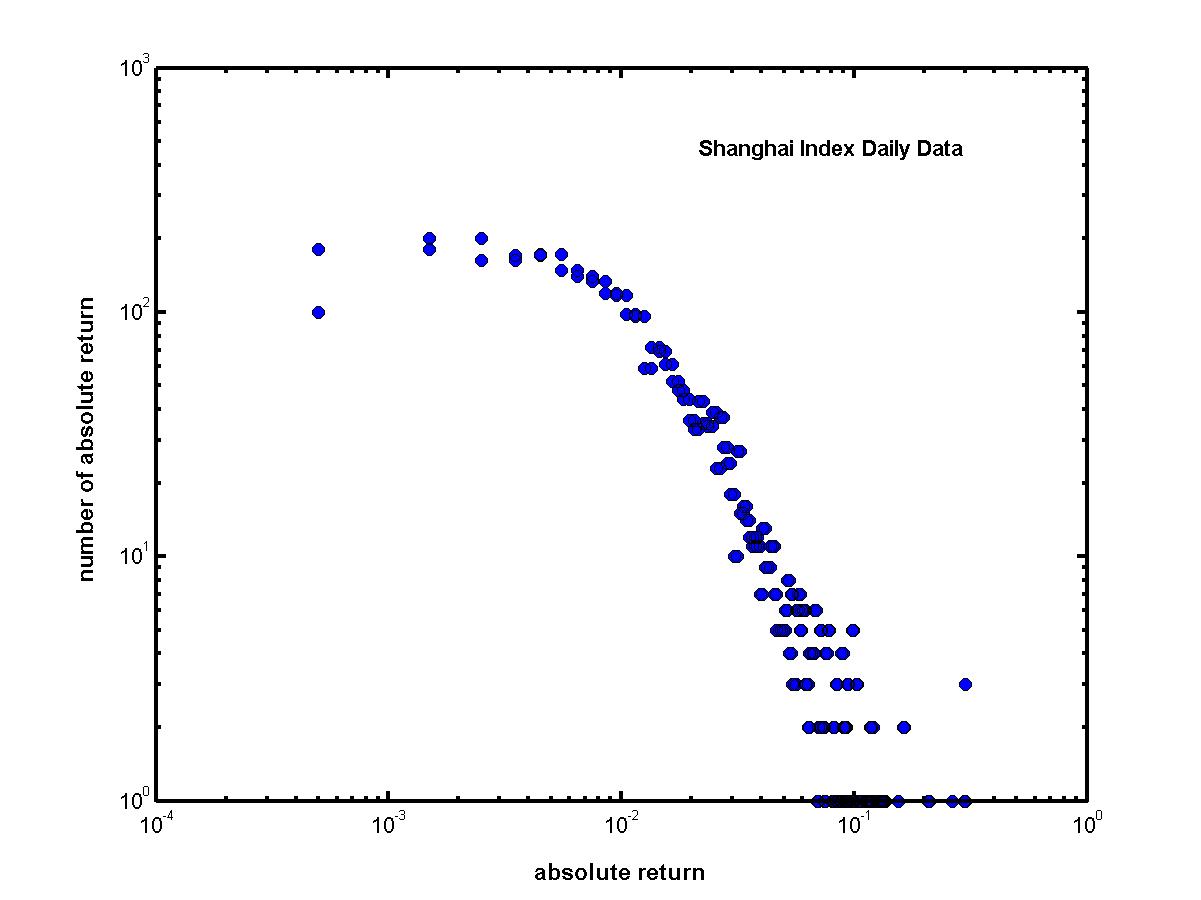

| Figure 6. Log-log plot of Shanghai Index daily absolute returns that is non-Gaussian (Yang 2004) |

|

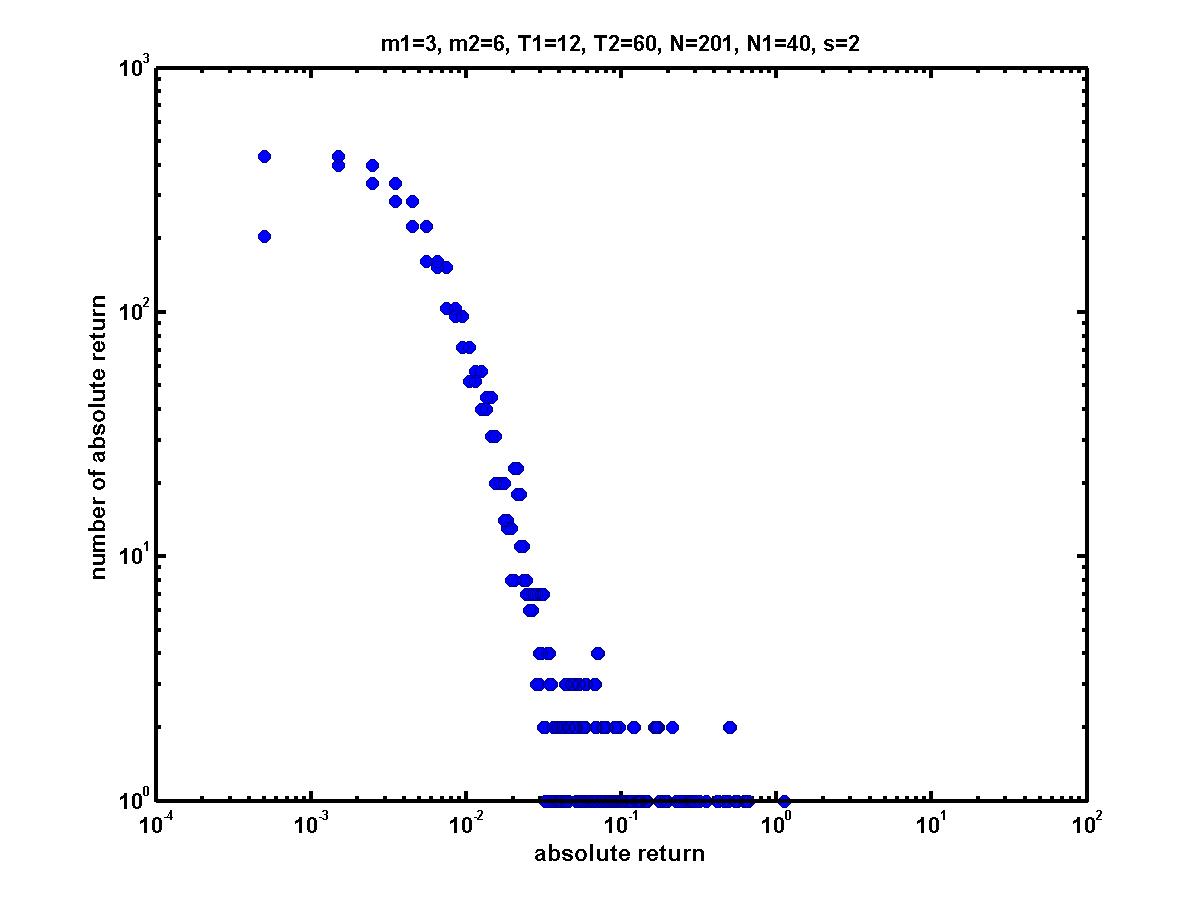

| Figure 7. Log-log plot of the mix-game absolute returns with parameters of m1=3, m2=6, T1=12, T2=60, N=201, N1=40 and s=2 |

|

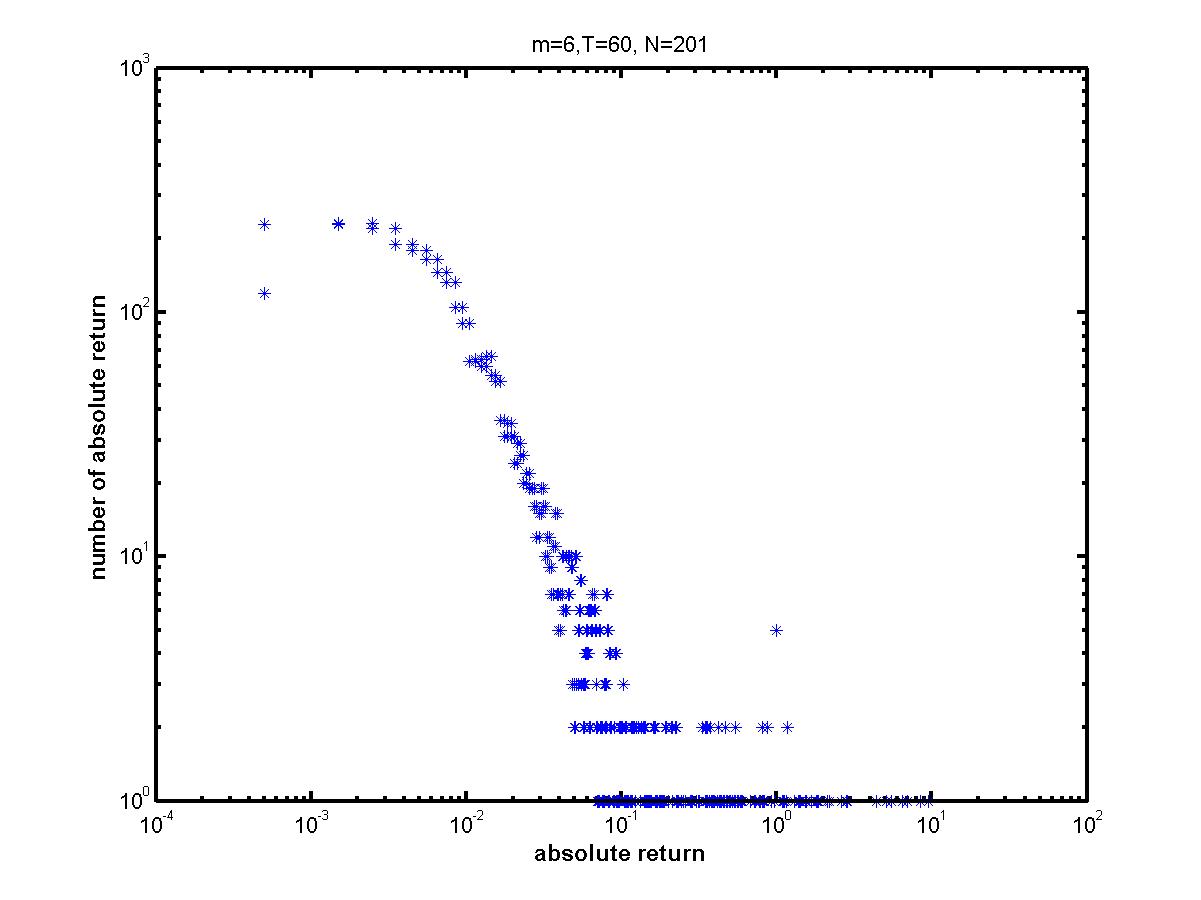

| Figure 8. Log-log plot of the MG absolute returns with parameters of m=6, T=60 and N=201 and s=2 |

|

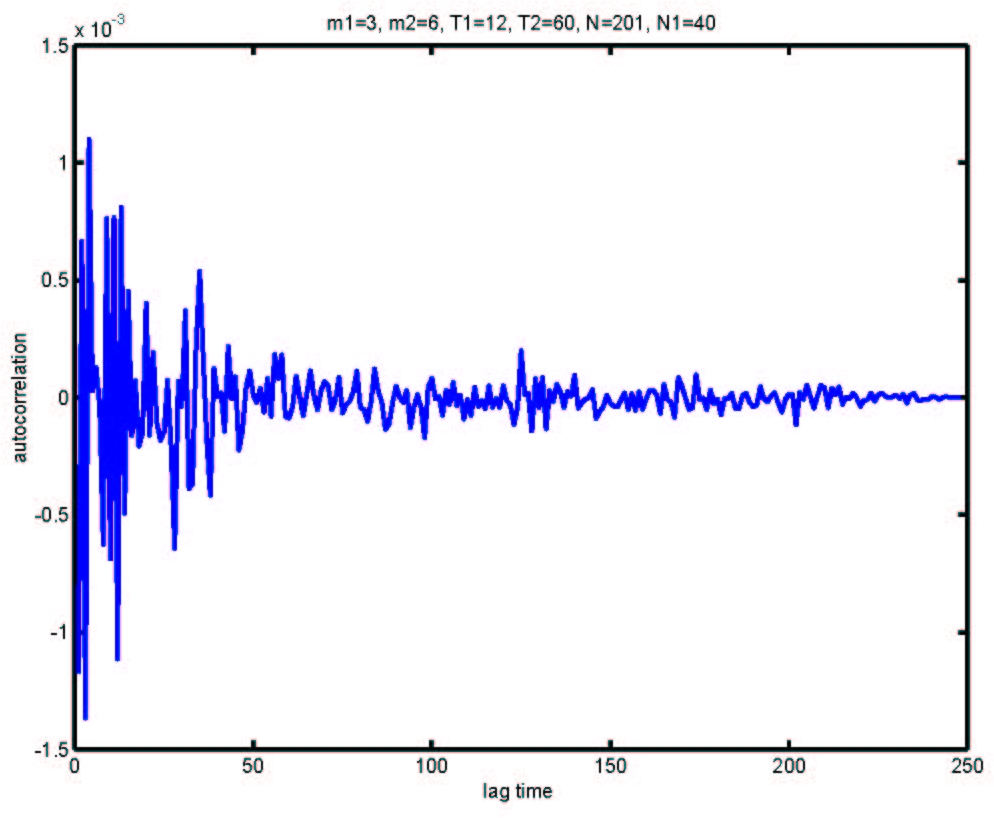

| Figure 9. Autocorrelations of logarithmic returns of the mix-game with m1=3, T1=12, m2=6, T2=60, N1=40, N=201 and s=2 |

| Table 4: A sample of agent's strategies (m=2) | |

| Historical information | prediction |

| 00 | 1 |

| 01 | 0 |

| 10 | 0 |

| 11 | 1 |

BOUCHAUD J.P. and Cont, R. (1998) Eur. Phys. J. B 6 543.

CHALLET, D. and Zhang, Y. C. (1997) Phyisca A 246, 407.

COOLEN A C C (2005) The Mathematical Theory of Minority Games, Oxford University Press, Oxford.

FARMER J.D. (2002) Industrial and Corporate Change vol. 11, 895-953.

GOU C. (2005) arXiv:physics/0508056.

GOU C. (2006) Chinese Physics 15 1239.

JEFFERIES P. and Johnson N. F. (2001) Oxford Center for Computational Finance working paper: OCCF/010702.

JOHNSON N. F., Hui P. M., Zheng D. and Hart M. (1999) J. Phys. A: Math. Gen. 32 L427-L431.

JOHNSON Neil F.,Jefferies P., and Hui P. M. (2003) Financial Market Complexity, Oxford University Press, Oxford.

JUDD K.L. and Tesfatsion L. edited (2005) Handbook of Computational Economics, Volume 2: Agent-Based Computational Economics, Elsevier Science B.V.

LUNA F. and Perrone A. edited (2002) Agent-based Methods in Economics and Finance: Sinulations in Swarm, Kluwer Academic Publisher, Norwell, Massachusetts.

LUX T. (1995) Economic Journal 105 881

LUX T. and Marchesi M. (1999) Nature 397 498

MARSILI M. (2001) Physica A 299 93.

SHLEIFER A. (2000) Inefficient Markets: an Introduction to Behavioral Financial, Oxford University Press, Oxford, UK.

YANG C. (2004) thesis of Beijing University of Aeronautics and Astronautics.

Return to Contents of this issue

Return to Contents of this issue

© Copyright Journal of Artificial Societies and Social Simulation, [2006]