Introduction and Literature Overview

The seminal paper by Nordhaus et al. (1992) applied a general equilibrium model to analyse the trade-off between economic growth and climate change; this approach has been extended to incorporate technological progress, heterogeneity and uncertainty. However, to assess the trade-off between these two potentially conflicting objectives (economic growth and climate change prevention), a family of Integrated Assessment models (IAMs) has been proposed, such as AIM (Kainuma et al. 1999), DEMETER (Gerlagh & Van Der Zwaan 2004), DICE (Nordhaus et al. 1992), ENTICE (Popp 2004), FUND (Tol 1997), IMAGE (Rotmans 2012), MERGE (Manne et al. 1995), MIND (Edenhofer et al. 2005), PAGE (Hope 2006), REMIND (Leimbach et al. 2010), RICE (Nordhaus & Yang 1996), and WITCH (Bosetti et al. 2006). For surveys, see Dowlatabadi (1995) on policy motivated integrated assessments of climate change, Kelly & Kolstad (1999) on methodologies applied, Stanton et al. (2009) on climate-economy models and Weyant (2017) on key challenges and areas for improvement. Moreover, Weyant (2017) (page 116) defines an

IAM of global climate change to be any model that encompasses the whole world and, at a minimum, includes some key elements of climate change mitigation and climate impacts systems at some level of aggregation.

For example, MIND[1], the Model of INvestment and endogenous technological Development, makes use of a macroeconomic approach and operates on aggregated economic values; technological progress and invest-ments are considered by funding the sectors (i) labour, (ii) fossil energy, (iii) fossil resource extraction, (iv) renew-able energy, (v) research and development, and (vi) carbon capturing and sequestration technologies. MIND admits dynamic optimisation of investments after a calibration of the productivity and sensitivity parameters, supported by empirical and theoretical parameter (interval) values. Extensions of MIND are, for instance, addressing uncertainty over selected parameters by chance constraint programming (Held et al. 2009), heterogeneous regions (Leimbach et al. 2010), value of learning (Lorenz et al. 2012), and cost-risk analysis (Neubersch et al. 2014). In the latter approach, the goal function includes a weighted sum of the welfare measure and the risk of exceeding the climate (temperature) target over the optimisation horizon. Furthermore, the trade-off parameter between social welfare and risk is calibrated within the cost-risk analysis. The IAM by Scheffran (2008) considers energy production technologies causing low or high carbon emissions within an adaptive optimisation process. Such a modelling approach can provide decision support to negotiate admissible emission trajectories and to better understand the choices of climate politics, including multiple agents and their interdependencies. Within the regional DICE model (RICE, Nordhaus & Boyer 2000), heterogeneity of regional impacts and income inequalities are investigated by Dennig et al. (2015), presenting estimates on the per capita consumption of the poorest agents (the lowest quantile) and showing the poorest in all regions can participate in economic growth when carbon pricing is optimal in a world with inversely proportional damage. Stern (2016), however, points out that the IAM class of models does not take all the relations among economics, social and environmental factors into account and fails to consider all of the consequences (e.g. potential conflicts, migrations as a result of sea level rise) in the decision evaluation, thus underestimating the uncertainty. Agent-Based Models (ABMs), by contrast, “seek to provide more realistic representations of socio-economics by simulating the economy through the interactions of a large number of different agents, on the basis of specific rules” (Stern 2016).

Balint et al. (2017) provide a survey of agent-based literature on the economics of climate change. In particular, they identify four areas in the relevant literature: (i) coalition formation and climate negotiations, (ii) macro-economic impacts of climate-related events, (iii) energy markets, and (iv) diffusion of climate-friendly technologies. In all of these areas, the impact of heterogeneity is one of the major research problems. For example, McGinty (2007) investigates the stability of coalitions of nations under heterogeneity. Lessmann et al. (2015) find that the heterogeneity of regions improves incentives to participate in climate agreements. Dosi et al. (2010) investigate the impact of public policies on heterogenous companies. In the family of LAGOM models (Haas & Jaeger 2005), heterogeneous households and producers facing climate-related risk are considered. Weber et al. (2005) develops a Multi-Actor Dynamic Integrated Assessment Model (MADIAM) which couples a climate change model (nonlinear impulse response model of a climate sub-system — NICCS) to an economic growth model (multi-actor dynamic economic model — MADEM). The adoption paths of climate-friendly technologies and the impact of heterogeneity in individual behaviours and preferences are studied in Windrum et al. (2009). In this context, Vona & Patriarca (2011) show that agent heterogeneity can hinder the diffusion of energy efficient technologies. The problem of the impact of heterogeneity on the diffusion of new technologies is also considered by Janssen & Jager (2002), Schwoon (2006), and Tran et al. (2013).

An agent-based approach provides the framework to consider the interplay of economic and climate-related problems. In this spirit, Lamperti et al. (2018) extend an agent-based macroeconomic model to include the climate-related aspects of economic growth at the global level and so provides the first agent-based integrated assessment model. The authors find that “climate damages from uncontrolled emissions are substantial and much more severe than predicted by many cost-benefit driven integrated assessment models” (Lamperti et al. 2018, 329). The modelling approach presented in this paper differs from theirs with respect to the specific agent types’ characteristic and behaviour. In general, the model presented in (Lamperti et al. 2018) focuses on technological growth and the financial sector, whereas our model is focused on the power generation and fuel extraction sectors. Our model is also limited to the real economy. Moreover, our model is calibrated based on real-world data and takes into account regional differences by considering ten different regions. Safarzyńska & van den Bergh (2017) analyse the interactions between technological, financial and energy systems. They consider heterogeneous agents: consumers, producers, power plants and banks. Ponta et al. (2018) investigate energy system transitions in the context of sustainable growth paths by using an extended version of the Eurace model. Geisendorf & Klippert (2017) investigates the effects of green investments within an agent-based climate-economy model and finds that IAMs cannot deal with the changing preferences or decision heuristics of the relevant agents.

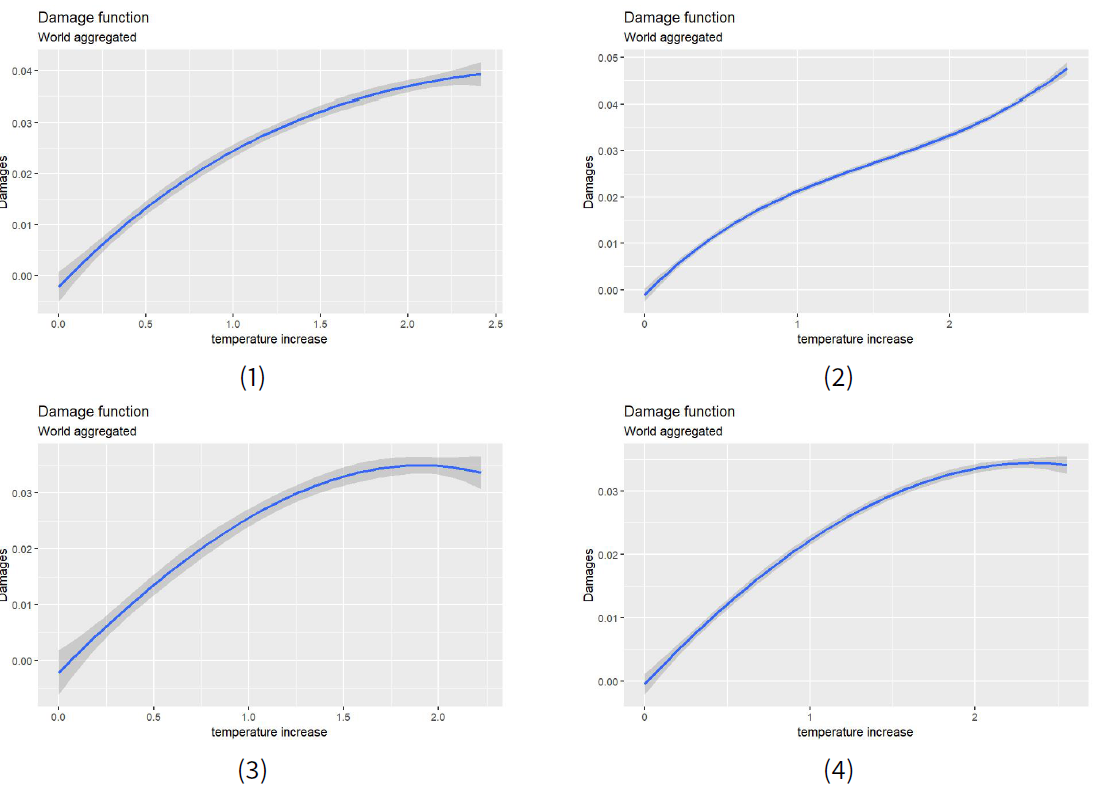

The economic impact of climate change is estimated using damage functions. These damage functions relate climatological quantities, such as temperature, sea level height and CO2 concentration, to economic damages in monetary terms (Diaz & Moore 2017). These damage functions are therefore a crucial component of IAMs. Covington & Thamotheram (2015) compares three widely used damage functions from Nordhaus (2013), Weitzman (2012) and Dietz & Stern (2015). As Figure 1 of Covington & Thamotheram (2015) demonstrates, the damage function produces a similar level of damage up to a 2 degree warming but differs widely for greater warming. An extensive discussion of damage functions is provided by National Academies of Sciences & Medicine (2017).

In our model we consider three types of damage. Damage to the agricultural sector, a decrease in labour productivity (Burke et al. 2015), and damage related to natural hazards related (see Coronese et al. (2019); Franzke (2017); Franzke & Czupryna (2019), for a more detailed discussion of this type of economic damage). The main contribution of this paper is to provide a bottom-up estimation of the shape of the relevant damage functions. The intermediate results are the GDP growth forecasts, with particular focus on energy sector development, for different scenarios with respect to the quantity of remaining fuel reserves and the dynamics of growth rates in renewable energy resources (primarily solar and wind). We also show that heterogeneity may play a significant role in such scenarios.

In the section entitled Model Overview, we introduce and provide the general description of the model. Implementation details are provided in the Model Details section. The simulation results, with an accompanying econometric analysis, are provided in the Results section. The findings and implications of our paper are summarised in the Conclusions section. The calibration methodology and the macroeconomic data used for the calibration are discussed in the dedicated Appendix.

Model Overview

With our model, we would like to address the following two research questions. Firstly: what is the relation between climate change, as measured by CO2 concentrations, and different economic growth scenarios? Secondly, what is the difference in the observed economic growth when we consider heterogeneous agents instead of homogeneous agents. Similarly, what is the difference when we consider the heterogeneous impact of dam-age upon agents, instead of the homogeneous impact? To answer these research questions, we construct an agent-based model (ABM) that focuses on the energy sectors and relevant climate facts in a detailed way, while combining it with consumer and capital goods, labour and capital markets modelled in a basic way. Fagiolo et al. (2007) lists four main characteristics of ABM models: a bottom-up perspective, heterogeneity, bounded rationality, and networked direct interactions. In our model, we first focus on autonomous decisions made by agents in the form of private households and companies, expressed in terms of planned activities relating to consumption and production respectively. Secondly, we consider different regions with a fixed number of agents in each region, but whose quantity may differ between regions. The agents cannot change their assigned region. In the first analysis which we present, all of the agents in a given region are homogeneous at the simulation start, but agents across two different regions may differ from each other. Additionally, agents in the same region may become different from each other (i.e. heterogenous) in subsequent rounds of the simulation. In the additional sensitivity analysis we also consider simulations with heterogeneous agents in the same region, right from the beginning of the simulation. Thirdly, all of the agents use simple heuristics for complex decisions having high levels of uncertainty, such as households planning the budget or companies deciding upon production levels. Finally, for consumer goods and capital goods, we consider local markets with customers directly linked to a subgroup of producers.

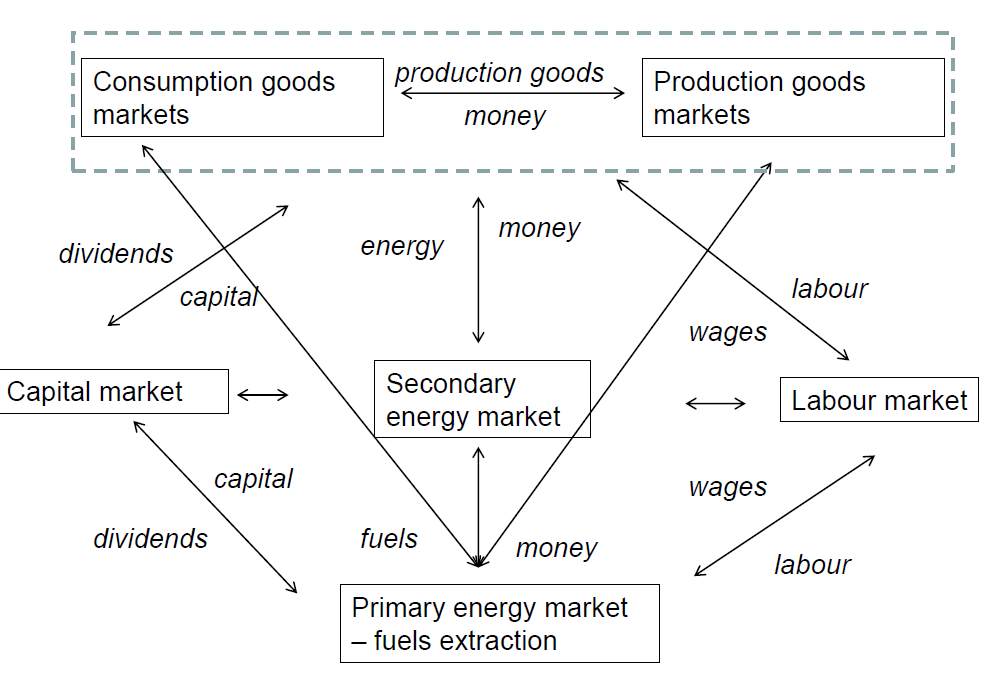

General framework

We consider the following agent types in our model, see 1:

- Citizens (private households)

- Energy sector companies

- Consumer goods companies

- Capital goods companies.

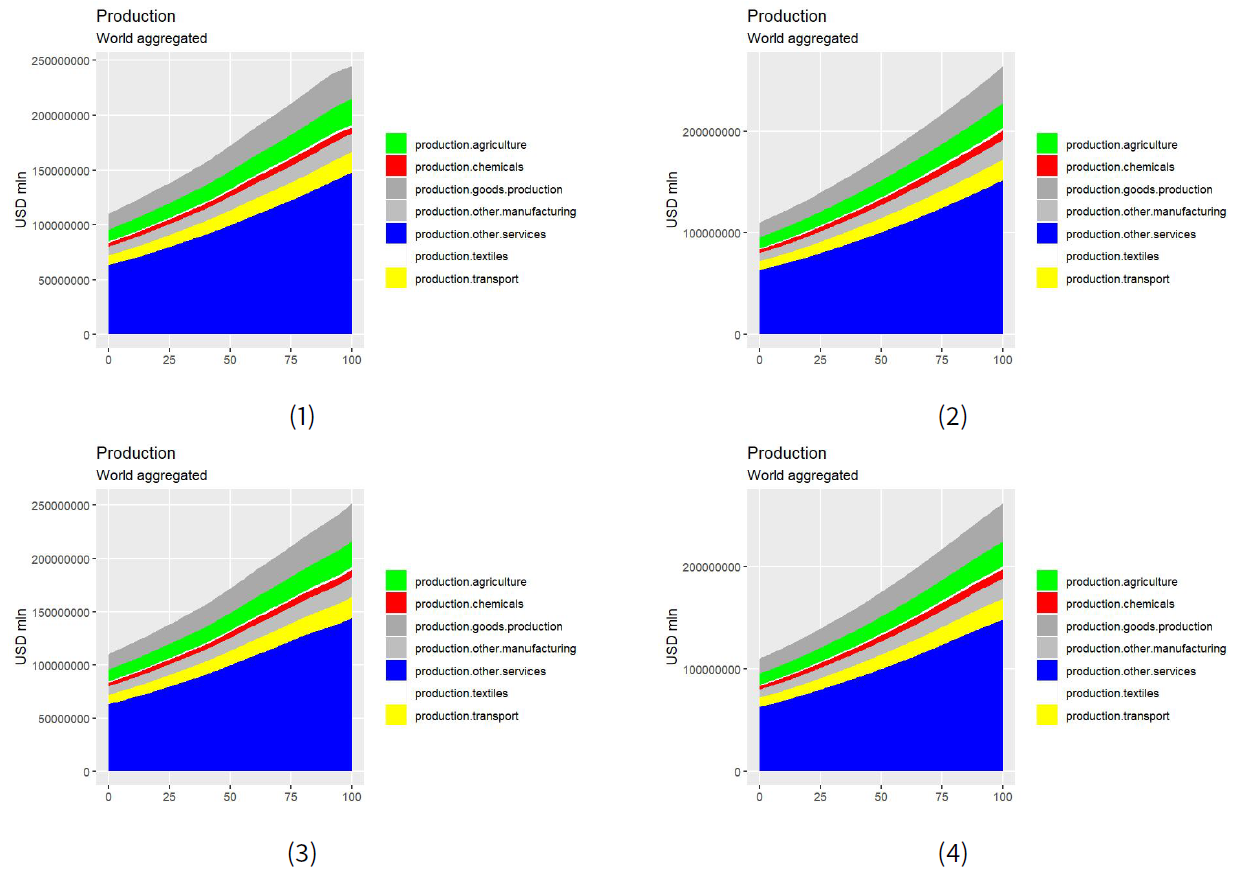

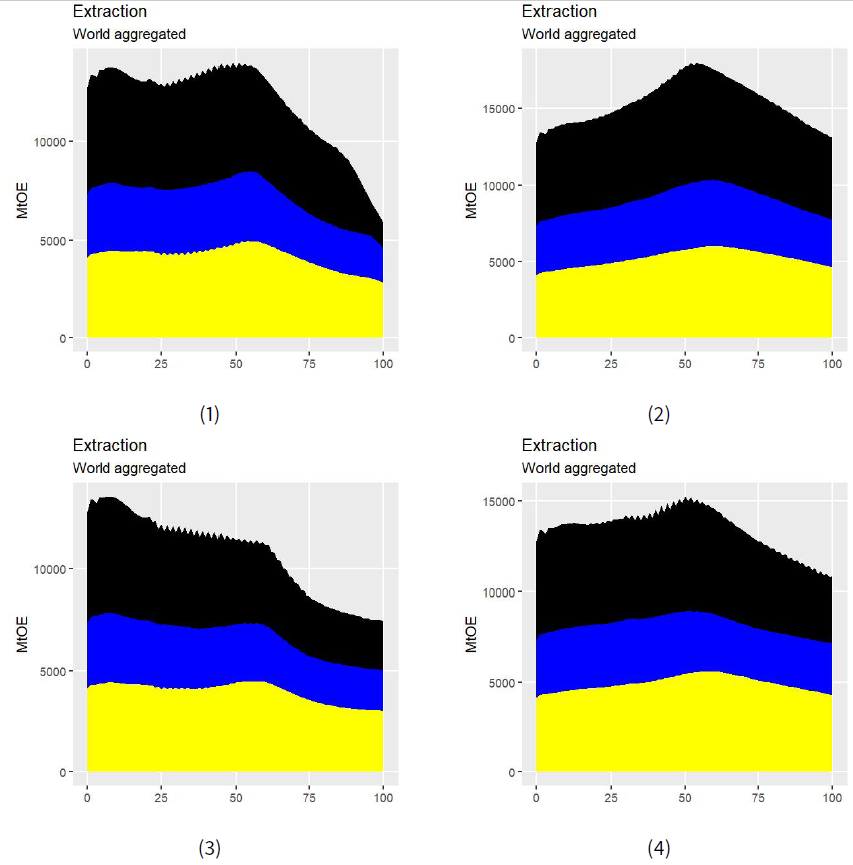

Consumer goods companies are further divided with respect to the goods produced within the following sectors: agriculture, textiles, chemicals, other manufacturing, transport and other services. We model the capital goods sector in a simplified manner as only one homogeneous capital good is considered in the model. The energy sector is subdivided into fuel extraction companies (with coal, gas and crude oil considered separately) and the electricity sector (power plants). As climate change influences different industry sectors in different ways (e.g. agriculture is the most sensitive sector to climate change) such subdivision enables us to consider the climate change effect for each sector individually.

Agents

Generally, we assume that agents optimise their behaviour when faced with relatively straightforward problems (the result depends mostly on the agent). However, when faced with more complex problems they use simple heuristics for the decision rules. A complex problem is taken to be a problem wherein the result depends on interactions with other agents or where a high degree of uncertainty prevails. Moreover, we assume that agents’ behaviour is subdivided into three phases. In the first phase, the agents update their state variables with the results of the market interactions with other agents. In the second phase, agents make forecasts of relevant market parameters, such as prices of goods, and plan their market behaviour accordingly. In the third and final phase, agents visit the relevant markets in the following order: capital, labour, fuel, electricity, capital goods and consumer goods, in order to buy or sell goods traded in these markets.

Agents use their next period (year) forecast of the gross domestic product (further abbreviated as GDP) growth rate to update their plans. Such forecasts are constructed under the assumption that real GDP growth rates can be described by the mean reverting process (Equation 1). This equation represents a discrete version of the Vasicek model, (Vasicek 1977) additionally limited from below by at the \(\textrm{min}_{\textrm{gdp}}\).

| $$f_{\textrm{gdp}} = max(\mu_{\textrm{gdp}} + \alpha_{\textrm{gdp}} \left(c_{\textrm{gdp}} - \mu_{\textrm{gdp}}\right) + \sigma_{\textrm{gdp}} \times \epsilon,\textrm{min}_{\textrm{gdp}})$$ | (1) |

We now briefly describe the agents used in the simulation, more details of which are provided in the next section.

Citizens

We first assume that private household preferences are represented by a Stone-Geary utility function (Stone 1954) with \(n\) consumer goods. The goal of citizens is to maximise their preferences, taking into account budgetary constraints. The budget available for consumption results firstly from a citizen’s income — labour wages and capital dividends — and secondly from his or her propensity to consume. The latter specifies how the total budget is divided between consumption and the purchase of new investments. The consumption budget is further divided according to the planned consumption of goods of different types, depending on agents’ preferences and the forecasted prices.

Energy sector companies - fuel extraction companies

We first assume that there is only one extraction company per geographical region and fuel type. We also assume that the marginal fuel extraction costs (and consequently the fuel prices also) depend on the cumulative extraction. This relation may be expressed as a Rogner curve (Nordhaus & Boyer 2000). The fuel extraction depends on the marginal cost of extraction and the physical capital available for a company. Due to the long investment period in this particular sector, we assumed that the fuel extraction company plans the necessary capital investments one period ahead. The company wants to increase the amount of physical capital available if the actual demand is higher than what was initially planned and decrease otherwise. Each company also has a production reserve.

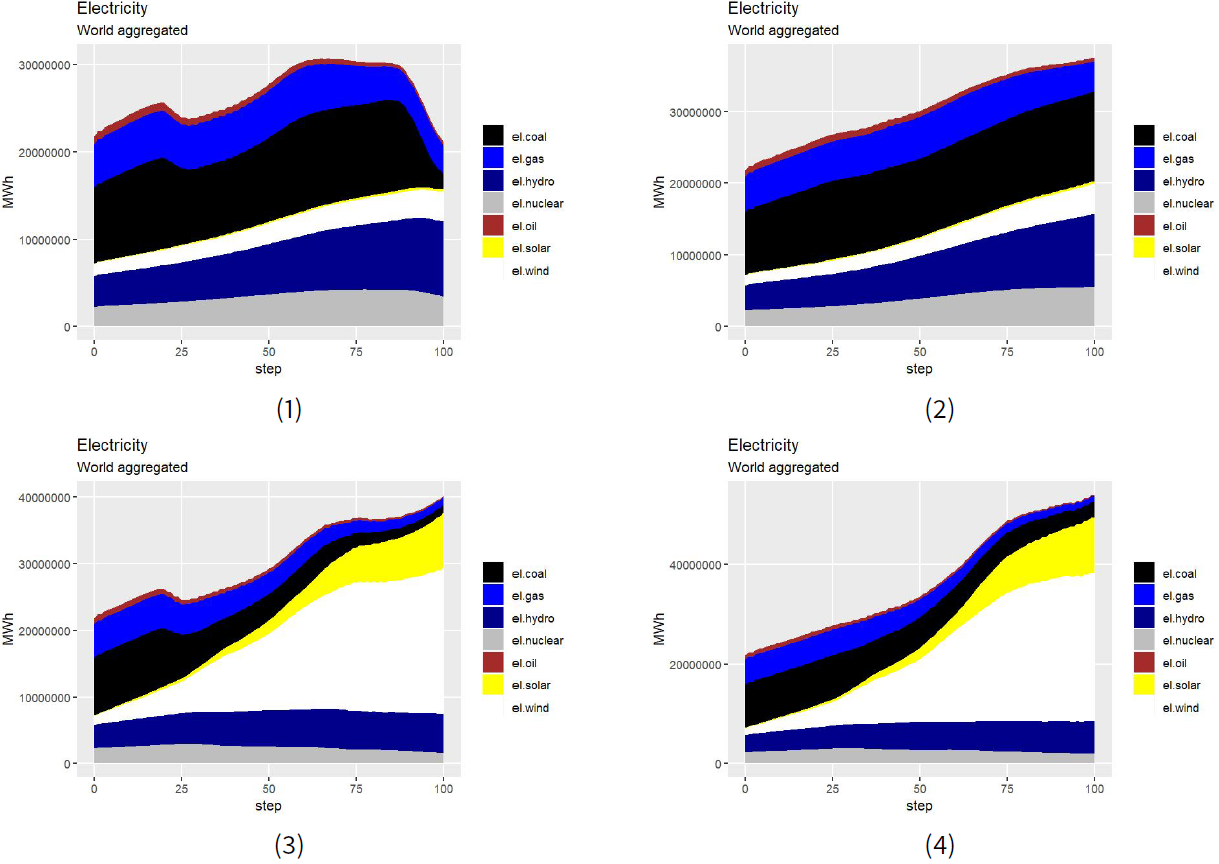

Energy sector companies – power plants

We consider the following power plant (electricity producer) types: coal, gas, oil, nuclear, hydro, wind, and so-lar. Each power plant is characterised by total capacity , a lifetime that depends on power plant type, a capacity factor which gives the average percent of time a given power plant is available, operations and management cost factor (refers to the total electricity produced before transmission losses and depends on the power plant type), electricity transmission loss factor and a conversion efficiency – the percentage of primary energy in fuel converted to electricity. Solar and wind power plants are additionally characterised by the storage capacity. A lifetime parameter is used for explicit modelling of the ageing of the installed capacities. The power plants adjust their capacities based on electricity demand and forecast GDP growth rates. We take the stochastic char-acter of electricity production (especially prominent in the case of renewable energy power plants) by using the parameterised Beta distribution.

Consumer goods companies

The technology of a consumer goods company is represented by a constant elasticity of substitution (CES) pro-duction function. The company uses capital, labour and energy as production factors. The goal of the company is to maximise its profit, calculated as the difference between revenue and the variable production costs (labour and energy costs). In the next simulation period, the planned production quantity and prices are set using sim-ple heuristics. The company adapts to changing demand and production costs. The necessary quantities of production factors are optimised so as to minimise the production cost yet still produce the planned production quantity. Profits are paid out in the form of a dividend to the owners (analogously, loss is covered by the owners) in return for the invested capital, which is primarily used for the purchase of the physical capital necessary for sustaining production.

Capital goods companies

Markets

We also consider the following markets:

- Capital markets

- Labour markets

- Fuel markets

- Electricity markets

- Capital goods markets

- Consumer goods markets

Capital markets

The capital market is demand driven. There is a separate market for each region. Private households invest in companies providing them with new capital. If the value of the new capital is higher than the capital goods demand (planned new investment and replacement investment), the surplus is redistributed among the owners. Otherwise, the planned capital goods demand is proportionally lowered. Although there is no debt market in our model, we allow for a negative cash reserve in the case of companies (similar to the case of private households).

Labour markets

The labour market is also modelled in a simplified way. Private households looking for employment are randomly matched with companies looking for employees. Companies fire employees if the planned labour requirements exceed the current labour force by more than one. We consider separate labour markets for different regions.

Fuel markets

fuel markets are modelled as centrally cleared markets, individually for each type of fuel considered in the model: coal, crude oil and gas. The fuel extraction companies offer the fuel at their marginal extraction cost with regular and maximal quantities (the difference is the production reserve)[2]. The fuel consuming agents (citizens, consumption and capital goods companies, power plants) bid the quantities and accept the market price (we assume that the demand for fuel is inelastic in the short term). The price results from the intersection of the supply curve and the vertical demand curve. The vertical shape of a demand curve represents the fact that the demand is inelastic in the short term.

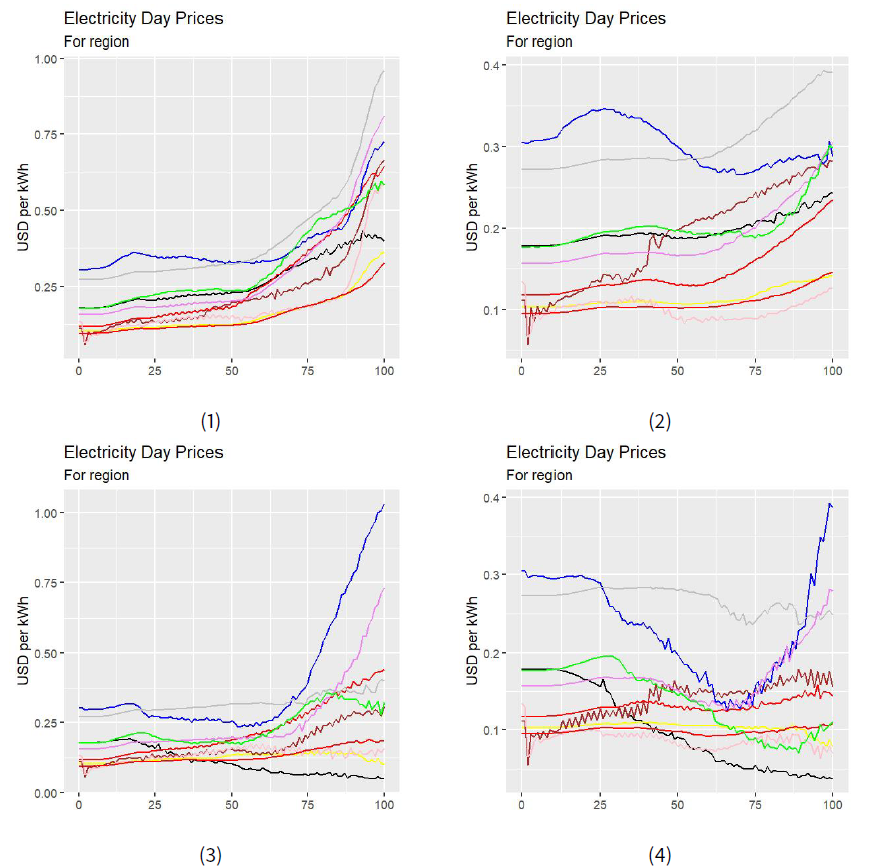

Electricity markets

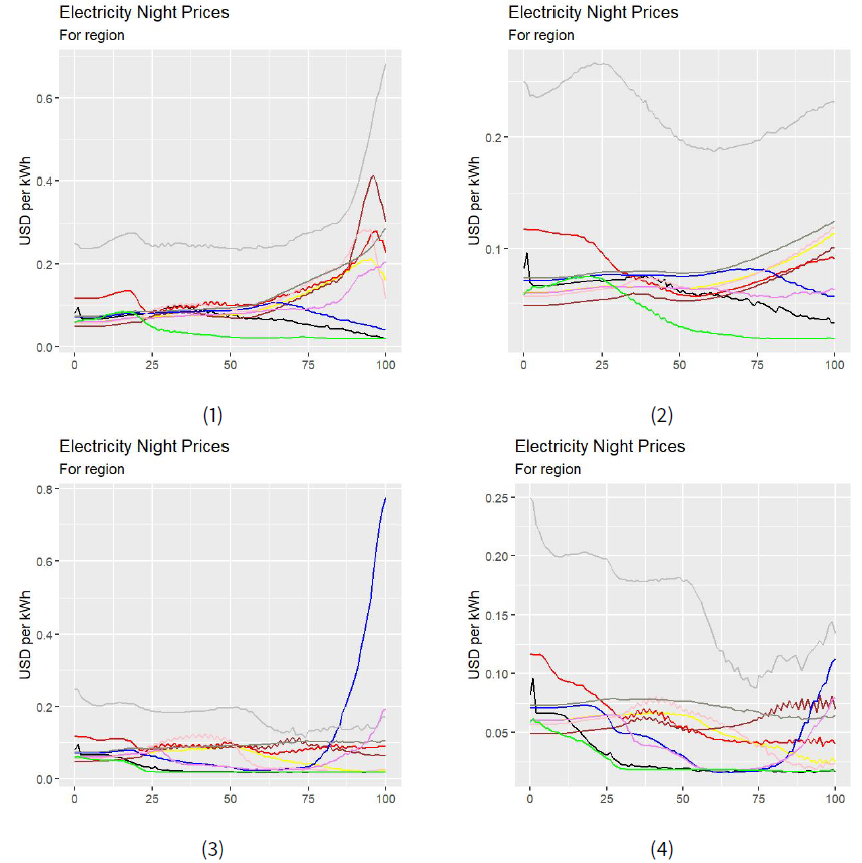

Electricity markets function in a similar way to the fuel markets but only on a regional level, rather than the global level that applies to fuel markets. Moreover, we consider a certain number of different electricity market clearing periods in a single simulation step. In this manner, we take into account the randomness in power generation, as power output from wind and solar plants may be different in each clearing period. To model the periodicity of electricity demand. we have introduced alternately changing periods of high and low electricity demand (we model the day and night demand regimes with peaks during daytime and lows at nighttime). We do not model seasonality of demand for reasons of simplicity.

Capital goods markets

The capital goods market is a global market but with local interactions. The demand side of the market con-sists of fuel extraction, electricity generation, capital goods companies and consumer goods companies. The demand for capital goods for a company equals the planned capital increase. The supply side consists of capital goods companies. The market is modelled in a simplified way, namely, we allow for capital goods companies to first produce the necessary capital increase for their own use. Furthermore, this portion of capital is available from the beginning of the simulation step. To model the local market — market fragmentation — we implement an adaptive approach with local interactions (Assenza et al. 2015). Each customer is connected to a certain number of producers (companies). A customer first buys from the connected producer that offers the lowest price. When the total demand exceeds the total supply of a company, the demand is only partly satisfied (in the same proportion for each customer). A customer with unsatisfied demand turns to the next connected company with the second lowest price, and so on.

Consumer goods markets

The consumer goods markets are modelled in an analogous way to capital goods markets. We have global markets for all sectors other than transportation and ‘other services’, which we consider as regional markets. The demand side of the market consists of citizens.

Damages

We consider the following types of damage related to global temperature increases: diminished productivity in an agricultural sector, diminished labour supply and efficiency, and natural disasters.

Time and space

We consider \(100\) discrete simulation steps, with each step representing one year. Moreover, we consider 10 geographical regions: Africa, Japan, China, India, Rest of Asia (including Australia and New Zealand), Europe, North America, Central and South America, Commonwealth of Independent States (CIS) and the Middle East. We have used the division of the World Trade Organisation, though China, India and Japan are treated separately to en-able comparability with the following models: RICE (Nordhaus & Boyer 2000) and REMIND (Leimbach et al. 2010). Each agent is assigned to only one of the regions considered in the model, so geographical factors are only implicitly, and in a simplified way, considered in our model.

Model Details

Model implementation details are provided in this section. We assume that the simulation step \(t\) is completed (agents planned their actions and visited all relevant markets where they interacted) and we discuss the next simulation step \(t+1\).

Citizens (private households)

In each step, a citizen first updates their state with the consequences of their market interactions with other agents (in the simulation step \(t\)). Then they plan their actions in the next period (in simulation step t+1). In particular, the agent collects a dividend, which is calculated as the sum of companies’ financial results in the simulation period \(t\) multiplied by the share of capital the agent holds in these companies, see Equation 2, where \(h_j^t\) is capital share in a company \(j\) and \(\pi_j^t\) its profit in period \(t\).

| $$\pi^t = \sum_{j=1}^{J} h_j^t \pi_j^t$$ | (2) |

Moreover, an agent similarly calculates the total expenditure for consumer goods as a sum of quantities of goods purchased and eventually consumed in the period \(t\) multiplied by their purchase prices, see Equation 3, where \(x_i\) is a quantity of good \(i\) consumed in period \(t\), and \(p_i^t\) its price.

| $$c^t = \sum_{i=1}^{n} x_i^t p_i^t$$ | (3) |

Then the savings from the previous period \(s_{t-1}\) are updated with the dividends and wages received, and the money spent on consumption in the simulation period \(t\), see Equation, where \(w^t\) is the wage earned over a period \(t\):

| $$s^t = s^{t-1} + w^t + \pi^t - c^t$$ | (4) |

In the planning phase, the agent first plans the prices. This is done in a simplified way by setting the planned price for the period \(t+1\) equal to the actual price observed in a period \(t\), namely setting \(\widetilde{p}^{t+1}_i= p^t_i\) for all goods other than electricity[3]. In the case of electricity, the planned price is calculated as an exponentially weighted moving average, with a parameterized weight \(w_{\textrm{el}}\).

| $$\widetilde{p}^{t+1}_{\textrm{el}} = w_{\textrm{el}} p^{t}_{\textrm{el}} + (1-w_{\textrm{el}}) \widetilde{p}^{t}_{\textrm{el}}$$ | (5) |

The agent then plans a total income during the period \(t+1\). Forecasts of both wage income and dividend payments are based on the current period values, increased in line with the forecasted GDP growth rate. Planned dividend income is calculated according to Equation 6.

| $$\widetilde{\pi}^{t+1} = \pi^t \times (1+ f_{\textrm{gdp}})$$ | (6) |

Additionally, the next period wage forecast also takes the regional unemployment rate into consideration. Namely, we assume that an unemployment rate value higher than \(s_{\textrm{unemp}}\), which is a simulation parameter, reduces the next period wage forecast to the value of the current period. For an unemployment rate equal to 0%, the next period wage forecast is calculated similarly to that of dividend income (planned wage growth rate is equal to planned GDP growth rate). For intermediate values of the unemployment rate — between 0% and \(s_{\textrm{unemp}}\), the planned wage growth rate is proportionally (linearly) decreased. Here we capture the stylized fact that the oversupply of the labour force reduces the increase in the price of labour (wage). We also assume that citizens always plan for a non-negative GDP growth rate in the susbequent period.

| $$\widetilde{w}^{t+1} = w^t \times (1+ f_{\textrm{unemp}} \times f_{\textrm{gdp}})$$ | (7) |

Eventually, the wage value will be increased using the nominal GDP growth rate \(r_{\textrm{gdp}}\) in the simulation period \(t+1\). As this variable can take on negative values (actual growth can be negative), some modifications are necessary. In particular, the factor \(f_{\textrm{unemp}}\) is modified for actual negative GDP growth rates in such a way that an unemployment rate higher than \(s_{\textrm{unemp}}\), which a simulation parameter, leads to a current period wage decrease equal to \(r_{\textrm{gdp}}\); an unemployment rate of 0% leads to no changes in the current wage and for intermediate (between 0% and \(s_{\textrm{unemp}}\)) values of the unemployment rate, the current wage reduction is determined by linear interpolation.

The agent also calculates planned total minimum consumption expenditure, see Equation 8.

| $$\widetilde{c}^{t+1}_{\textrm{min}} = \sum_{i=1}^{n} x_i^{\textrm{min}} \widetilde{p}_i^{t+1}$$ | (8) |

Accordingly, the total minimum income available (such an income that enables just a minimum consumption for a given propensity to consume value, modelled using a propensity to consume parameter – \(a\)) is planned, see Equation 9:

| $$\widetilde{i}^{t+1}_{\textrm{min}} = \left(\widetilde{c}^{t+1}_{\textrm{min}}\right)^{1/a}$$ | (9) |

A household \(l\) plans total available income \(\widetilde{i}^{t+1}\) as the sum of planned wage income and planned dividend payments, see Equation 10.

| $$\widetilde{i}^{t+1} = max(\widetilde{w}^{t+1} + \widetilde{\pi}^{t+1},\widetilde{i}^{t+1}_{\textrm{min}} )$$ | (10) |

Then a citizen \(l\) decides on the next period’s planned total consumption level, depending on the propensity to consume \(a \in [0,1]\), in two steps, see Equations 11 and 12. In the first step, planned consumption for period \(t+1\) is calculated as a certain proportion of the planned income for period \(t+1\).

| $$\widetilde{c}^{t+1}_0 = \left(\widetilde{i}^{t+1}\right)^{a}$$ | (11) |

In the second step, the overall consumption level is corrected by the savings component (cash at hand) by adding:

| $$\widetilde{c}^{t+1} = max(\widetilde{c}^{t+1}_0 + \alpha_{\textrm{savings}} \times \left(s^{t} - s^{0} \right), \widetilde{c}^{t+1}_{\textrm{min}})$$ | (12) |

Equation 12 represents the behaviour of households that plan to spend part of their accumulated cash by gradually increasing their planned consumption level or, conversely, plan to increase cash holdings (in the case where it is decreased) by gradually reducing planned consumption. We use a parameter \(\alpha_{\textrm{savings}}\) to model this behaviour. Note that usage of the terms ’savings’ and ’investments’ deviate from the standard economic approach: private households use savings to transfer money to the next time period, without any kind of interest accruing. The investments by private households to companies generate a dividend payment in the future. The difference between planned income and planned consumption gives the values of planned total investments, see Equation 13.

| $$\widetilde{o}^{t+1} = \widetilde{i}^{t+1} - \widetilde{c}^{t+1}$$ | (13) |

In the next step, total planned consumption is decomposed into different types of goods. As noted in the introduction, we model seven consumer goods sectors, such that \(n = 7\). For this purpose we assume that private household preferences are represented by a Stone-Geary utility function (Stone 1954) with \(n\) consumer goods:

| $$U_{l}(x_{1},\dots, x_{n})=\prod_{i=1}^{n}(x_i-x_i^{min}) ^{\alpha_i}\\$$ | (14) |

| $$\widetilde{x}^{t+1}_k = x_k^{min} + \alpha_k/ \widetilde{p}^{t+1}_k \times (\widetilde{c}^{t+1} - \sum_{i=1}^{n} x_i^{min} \widetilde{p}^{t+1}_i ), \forall k\in \{1,\dots, n\} \\$$ | (15) |

Hence, given that all basic needs \(x_{k}^{min}\) are fulfilled, the remaining amount for consumption, \(\widetilde{c}^{t+1} - \sum x_i^{min} \widetilde{p}^{t+1}_i\), is spent according to the ratio of the preference weighting \(\alpha_k\) and the planned price \(\widetilde{p}^{t+1}_k\).

The planned total energy consumption \(\widetilde{x}^{t+1}_7 = x_{ec}\) is first decomposed into electricity and energy from fuels, and then the energy obtained directly from fuels is further decomposed into energy from coal (solid fuel), gas (gaseous fuel) and crude oil (liquid fuel), using the nested Constant Elasticity of Substitution (CES) functions (we further skip indexation by period \(t+1\) for the sake of clarity ):

| $$x_{e} = ((\eta_{el} x_{el})^{\rho_{e}} + (\eta_f x_f)^{\rho_{e}})^{1/\rho_{e}} \\$$ | (16) |

| $$x_f = ((\eta_{coal} x_{coal})^{\rho_f} +(\eta_{gas} x_{gas})^{\rho_f}+(\eta_{oil} x_{oil})^{\rho_f} )^{1/\rho_f} \\$$ | (17) |

| $$x_{el} = \frac{x_e}{\eta_{el}} \times \frac{{\left(\frac{p_{el}}{\eta_{el}}\right)}^{\frac{1}{\rho_{e}-1}}} {{\left({\left(\frac{p_{el}}{\eta_{el}}\right)}^{\frac{\rho_{e}}{\rho_{e}-1}} + {\left(\frac{p_{f}}{\eta_{f}}\right)}^{\frac{\rho_{e}}{\rho_{e}-1}} \right)}^\frac{1}{\rho_{e}}}$$ | (18) |

Capital decisions are modelled in the following simplified way. The planned capital investments \(\widetilde{o}^{t+1}\) are divided by a citizen into separate companies \(j\) based on the current portfolio of shares in different companies and the values of the companies’ planned capital increase, according to Equation 19.

| $$\widetilde{o}^{t+1}_j=\frac{h_j^t \widetilde{\Delta k}^{t+1}_j}{\sum_{i=1}^{J} h_i^t \widetilde{\Delta k}^{t+1}_i} \times \widetilde{o}^{t+1}$$ | (19) |

\(\widetilde{o}^{t+1}_j\) stands for the total value of new capital that is planned for investment in company \(j\) in the next period \(t+1\) by a private household. \(h_j^t\) is the current share of the total capital invested in company \(j\) that is owned by a particular citizen. In general, a company may be owned by many citizens. \(\widetilde{\Delta k}^{t+1}_j\) is the total (physical) capital increase planned by company \(j\) in the period \(t=1\). Its value is calculated by multiplying with \(\bar{p}_{pg}^t\), which is the average price of the capital goods in period \(t\) in the simulation. The symbol \(\widetilde{o}^{t+1}\) denotes total planned investments in the period \(t+1\). This mechanism represents a simplification and captures the fact that the planned investments in company \(j\) is proportional to the company’s capital requirements and the value of current capital already invested in the company (ownership 'bias').

Consumer goods company

In each step, a consumer goods company first updates its state with the consequences of the market interactions with other agents (in the already completed simulation step \(t\)). Then it plans its actions for the next period (in simulation step \(t+1\) which just began, all agents first plan their actions). Firstly, the financial result based on cash flow is calculated by deducting variable production costs from revenues, as shown in Equation 20, where \(d^t\) is the total demand in period t, \(y^t\) is the total production in the same period, \(\textrm{st}^{t-1}\) represents stocks at the end of the given period \(t-1\), \(p^t\) is the unit price, \(\bar{w}^t\) the average wage offered, \(l^t\) the number of employees, \(e^t\) the total energy used in period \(t\) and \(p_e^t\) the mean price of this energy.

| $$\pi^t_0 = p^t min\left(d^t,y^t - (\textrm{st}^{t} - \textrm{st}^{t-1})\right) - \bar{w}^tl^t - p_e^t e^t$$ | (20) |

Moreover, the cash surplus is calculated as the difference between money for investments collected from citizens in period \(t\) and the value of the actual investments — the difference between capital value after depreciation at the end of period \(t-1\) and the capital value before depreciation at the end of period \(t\) — in this period \(\Delta \textrm{kv}^t = \textrm{kv}^t - \textrm{kv}_d^{t-1}\), as shown in Equation 21, where \(\widetilde{o}^{t}_{ji}\) is the money planned for investment in company \(j\) by citizen \(i\) in period \(t\).

| $$\pi^t_1 = \sum_{i=1}^{i=m} \widetilde{o}^{t}_{ji} - \Delta \textrm{kv}^t$$ | (21) |

The total dividend to be distributed among owners in period \(t\) is calculated as the sum of \(\pi^t = \pi^t_0 + \pi^t_1\).

A company also calculates the average production cost as Equation 22

| $$\bar{c}_p^t = \frac{\bar{w}^tl^t + p_e^t e^t}{y^t}$$ | (22) |

Depending on the relation of the current price \(p^t\) to the average market price \(\bar{p}^t\) and of demand \(d^t\) to production \(y^t\) and the average production cost \(\bar{c}_p^t\), the planned price and production in the next period \(t+1\) are adjusted in the following way, see (Assenza et al. 2015):

- if \(p^t \le \bar{p}^t\) and \(d^t < y^t\) then production is decreased

- if \(p^t \le \bar{p}^t\) and \(d^t \ge y^t\) then price is increased

- if \(p^t > \bar{p}^t\) and \(d^t < y^t\) then price is decreased

- if \(p^t > \bar{p}^t\) and \(d^t \ge y^t\) then production is increased

As an example, the necessary adjustments are shown in Equation 23 for the first case and Equation 24 for the second case, where \(\nu\) is a uniformly distributed random variable. \(f_{\textrm{price}}\) and \(f_{\textrm{prod}}\) are the simulation parameters. Additionally, \(f_{\textrm{price}}\) limits the maximum price increase. This additional restriction limits excessive price fluctuations resulting from changes in the prices of production prices (it expresses a certain level of conservatism in the price-setting mechanism by companies).

| $$\begin{split} \widetilde{p}^{t+1} = \textrm{min}(\textrm{max}(p^t,\bar{c}^t ),p^t(1+f_{\textrm{price}})) \\ \widetilde{y}^{t+1} = y^t (1+f_{\textrm{gdp}}) (1+f_{\textrm{prod}} \nu) \end{split}$$ | (23) |

| $$\begin{split} \widetilde{p}^{t+1} = \textrm{min}(\textrm{max}(p^t (1+f_{\textrm{price}}\nu),\bar{c}^t ),p^t(1+f_{\textrm{price}})) \\ \widetilde{y}^{t+1} = y^t (1+f_{\textrm{gdp}}) \end{split}$$ | (24) |

Other prices are planned similarly to the case of households, see Equations 7 and 5. The cost of capital is set to the value of the depreciation rate \(f_{\textrm{depr}}\). At the end of each period, capital is depreciated according to the formula in Equation 25.

| $$k_d^t = k^t \times (1-f_{\textrm{depr}})$$ | (25) |

The production function is a CES function with the following production factors: capital \(k\), labour \(l\) and energy, denoted by symbol \(e\):

| $$y_j = ((\eta_{k} k)^{\rho_y} +(\eta_{l} l)^{\rho_y}+(\eta_{e} e)^{\rho_y} )^{1/\rho_y} \\$$ | (26) |

The company minimises its production cost given the planned production in the next period \(\widetilde{y}^{t+1}\) and the assumed values of the CES production function. The quantities of the necessary production factors — capital, labour and energy — are shown in Equation 27.

| $$\begin{split} d={\left({\left(\frac{f_{\textrm{depr}}}{\eta_{k}}\right)}^{\frac{\rho_{y}}{\rho_{y}-1}} + {\left(\frac{\widetilde{w}^{t+1}}{\eta_{l}}\right)}^{\frac{\rho_{y}}{\rho_{y}-1}} + {\left(\frac{\widetilde{p}_e^{t+1}}{\eta_{e}}\right)}^{\frac{\rho_{y}}{\rho_{y}-1}} \right)}^\frac{1}{\rho_{y}} \\ \widetilde{k}^{t+1}= \frac{\widetilde{y}^{t+1}}{\eta_{k}} \times \frac{{\left(\frac{f_{\textrm{depr}}}{\eta_{k}}\right)}^{\frac{1}{\rho_{y}-1}}}{d} \\ \widetilde{l}^{t+1}= \frac{\widetilde{y}^{t+1}}{\eta_{l}} \times \frac{{\left(\frac{\widetilde{w}^{t+1}}{\eta_{l}}\right)}^{\frac{1}{\rho_{y}-1}}}{d} \\ \widetilde{e}^{t+1}= \frac{\widetilde{y}^{t+1}}{\eta_{e}} \times \frac{{\left(\frac{\widetilde{p}_e^{t+1}}{\eta_{e}}\right)}^{\frac{1}{\rho_{y}-1}}}{d} \\ \end{split}$$ | (27) |

Energy demand for electricity and energy from solids (coal, gas and oil) is modelled by the nested CES function in a similar way to that of private households. The company minimises its production and energy cost, providing the required level of planned production.

A consumer goods company goes bankrupt if it is not able to continue production. This may result from lack of demand or lack of necessary production factors. In this case, the owners cover possible losses.

Capital goods company

Capital goods companies are subject to similar mechanisms as consumer goods companies. The major difference is that the company may produce the physical capital (production factor) for its own use.

Fuel extraction company

The fuel extraction company in our model is fundamentally subject to similar mechanisms as the consumer goods company. Therefore, we will limit the description here to the specific differences relative to consumer goods companies. Since the fuel extraction sector is generally considered to be strategic by governments, and it is typically either heavily regulated or state-owned, we model the fuel extraction company in a simplified way. First, we assume that there is only one extraction company per geographical region and fuel type. Second, we assume that the marginal fuel extraction costs (and thus the fuel price also) depend on the cumulative extrac-tion. This relation may be expressed as a Rogner curve (Nordhaus & Boyer 2000). We model extraction company production using the calibrated Rogner curve, as done in the MIND model, (Edenhofer et al. 2005). To be more precise, the marginal fuel extraction costs are given by Equation 28, where \(\chi_1\), \(\chi_2\), \(\chi_3\) and \(\chi_4\) are the parameters of the calibrated Rogner curve. The parameters \(\chi_1\) and \(\chi_3\) both have a straightforward economic interpretation. Namely, \(\chi_1\) is the initial (at the beginning of the simulation) price of the fuel and \(\chi_3\) equals the total regional fuel reserves remaining. \(Y\) is the accumulated fuel resource extraction since the simulation began.

| $$c_m =\chi_1 + \chi_2 \left({\frac{Y}{\chi_3}}\right)^{\chi_4}$$ | (28) |

Third, we assume that the fuel extraction company holds more capital than required to extract the planned amount of fuel, and maintains production reserves. For example, similar behaviour can be observed for OPEC countries, where the production potential is higher than current production.

The financial result — based on cash flow — is calculated as shown in Equation 29, where \(d^t\) represents total demand in period t, \(y^t\) is total production in the same period, \(\textrm{st}^{t-1}\) represents the stocks available at the end of the given period \(t-1\), \(p^t\) is the unit price, \(\bar{w}^t\) the average wage offered, \(l^t\) denotes number of employees, and \(\textrm{sub}^t\) is the sum of the subsidy granted to the local power plant fired with this particular type of fuel.

| $$\pi^t_0 = p^t \textrm{min}\left(d^t,y^t-(\textrm{st}^{t} - \textrm{st}^{t-1})\right) - \bar{w}^t l^t - \textrm{sub}^t$$ | (29) |

In the Middle East and Asia regions the observed electricity prices are at such a low level that they do not even cover the costs of fossil fuels used for their production. Local power plants can buy the fuels (gas and crude oil) below the world market price. We model this observation by moving part of the earnings from fuel extraction companies to the regional electricity companies in the form of subsidies.

Due to the long investment period applicable to this particular sector, we assumed that the fuel extraction company plans the necessary capital allocation one period ahead[4] depending on actual demand in period \(t\), denoted \(d^t\), initially planned demand for period \(t\), denoted \(\widetilde{d}^t\), and a forecast GDP growth rate for the second consecutive period, denoted \(f^1_{\textrm{gdp}}\). Additionally, \(\nu\) is a uniformly distributed random variable and \(f_{\textrm{prod}}\) is the simulation parameter. The company wants to increase the amount of physical capital available if the actual demand is higher than what was initially planned or decrease it otherwise. The prolonged investment period enables the fuel markets to clear before capital goods markets during the simulation.

| $$\begin{split} d^t<\widetilde{d}^t: \widetilde{k}^{t+1} =k^t (1+f^1_{\textrm{gdp}}) (1- \nu f_{\textrm{prod}} ) \\ d^t=\widetilde{d}^t: \widetilde{k}^{t+1} =k^t (1+f^1_{\textrm{gdp}}) \\ d^t>\widetilde{d}^t: \widetilde{k}^{t+1} =k^t (1+f^1_{\textrm{gdp}}) (1+ \nu f_{\textrm{prod}}) \\ \end{split}$$ | (30) |

Then the production supply and demand prices for period \(t+1\) are planned in five steps.

- The current value of the marginal extraction cost \(c_m^t\) is calculated according to Equation 28. Second, the planned production for period t+1 is calculated as given in Equation 31

| $$\widetilde{y}^{t+1}_j = \frac{\chi_1}{c_m^t} \times k^{t} \times \textrm{kp} \times (1-\textrm{rr})$$ | (31) |

- We initially considered the individual and independent fuel extraction for each region. However different regional values for the ratio: total accumulated fuel extraction to initial (at simulation start) total fuel reserves remaining (fuel reserve depletion rates) observed in the different regions led to different planned prices between regions. Generally, we can expect that more easily accessible fuel deposits will be extracted first. As the fuel markets are global, we can also expect that fuel extraction will have an additional tendency to move from regions with higher depletion rates to those with lower depletion rates. We model this observation by additionally multiplying planned production by the factor defined by Equation 32, where \(j\) denotes a region, \(J\) is the number of fuel extraction companies, \(y_j\) denotes for planned fuel extraction, \(Y_j^t/\chi_{3,j}\) is the regional exhaustion rate and \(\textrm{con}_{\textrm{fuel}}\) the extraction convergence factor, which is used as a simulation parameter. At the end of the process, the planned production values are proportionally adjusted so that global planned production, before and after scaling with the factor defined in Equation 32, remains the same.

| $$1 + \left(\frac{\sum_{j=1}^{J} \widetilde{y}^{t+1}_j \times \frac{Y_j^t}{\chi_{3,j}}}{\sum_{j=1}^{J}\widetilde{y}^{t+1}_j} - \frac{Y_j^t}{\chi_{3,j}} \right) \times \textrm{con}_{\textrm{fuel}}$$ | (32) |

- The maximum production in period \(t+1\) is calculated as in Equation 33.

| $$\widetilde{y}_{\textrm{max}}^{t+1} = \frac{\widetilde{y}^{t+1}}{1-\textrm{rr}}$$ | (33) |

- The planned price is set to the current value of the marginal extraction cost \(\widetilde{p}^{t+1}=c_m^t\).

- Planned demand is set to the value of planned production \(\widetilde{d}^{t+1} = \widetilde{y}^{t+1}\).

The number of employees remains constant until all available resources are exhausted. This is a simplifying assumption, since labour is not explicitly used as a production factor but is only assigned, based on the empirical values for each individual company. The fuel extraction company goes bankrupt if all the resources are exhausted. In this case, the owners cover possible losses.

Electricity company

We consider the following power plant (electricity producer) types: coal, gas, oil, nuclear, hydro, wind, and solar. Each power plant is characterised by a total capacity \(c_p^t\), an additional term for storage capacity \(c_s^t\) in the case of solar and wind power plants, a lifetime that is dependent on power plant type \(T\), a capacity factor \(f_{\textrm{capacity}}\) giving the average percentage of time a given power plant is available, an operations and management cost factor \(f_\textrm{om}\) (refers to the total electricity produced before transmission losses and depends on the power plant type), electricity transmission loss factor \(f_{\textrm{eloss}}\) and the conversion efficiency \(f_\textrm{conveff}\) — the percentage of primary energy in fuel converted to electricity. A lifetime \(T\) is used for explicit modelling of the ageing of the installed capacities — each part of the installed power plant capacity is characterised by age and is removed (depreciated) at the age of \(T\).

For each simulation step, we consider \(N_e\) electricity market sub-steps with separate clearing. We use finer time gradations for electricity markets in order to model the stochastic power generation profiles for different power plant types. First, at the beginning of the simulation step, a power plant updates the total electricity produced (corrected for electricity transmission losses) in step \(t\), denoted \(y^t\), see Equation 34 and the average price, denoted \(\bar{p}^t\).

| $$\begin{split} y^t=\sum_{i=1}^{N_e} y_i^t \\ y^t_{\textrm{max}}=max(y_1^t,y_2^t,...,y_{N_e}^t) \\ \end{split}$$ | (34) |

| $$\begin{split} y_t>0: \bar{p}^t=\frac{\sum_{i=1}^{N_e} y_i^t p_i^t}{\sum_{i=1}^{N_e} y_i^t} \\ y_t = 0: \bar{p}^t=\frac{\sum_{i=1}^{N_e} p_i^t}{N_e} \\ \end{split}$$ | (35) |

The financial result — based on cash flow — is calculated as the difference between income and production cost, details are presented in Equation 36, where \(f_{\textrm{om}}\) is operations and management cost factor, \(x_f^t\) the fuel used for electricity production, and \(p_f^t\) its price. \(x_s^t\) denotes settlement cost, which is discussed later in greater detail. We assumed that in such regions as the Middle East and Asia, gas and crude oil prices used for electricity production are subsidised, with \(f_{\textrm{sub}}\) being the subsidy rate.

| $$\pi^t_0 = y^t \bar{p}^t - \frac{y^t}{1-f_{\textrm{eloss}}} f_{\textrm{om}} - p_f^t (1-f_{\textrm{sub}}) + x_s^t$$ | (36) |

There are more power plants (the number of power plants in the simulation was decided according to typical power plant capacity) than citizens[5] working in the electricity sector in the simulation model. In order to avoid the partial allocation of employees to specific power plants, citizens are only allocated to the electricity sector as a whole but not to a particular power plant. Such a partial allocation of employers would represent the possibility of a citizen working in many power plants simultaneously, which we avoided for reasons of simplicity. As a consequence, the operations and management (O&M) cost at the power plant level are calculated in a different way than for the sector as a whole — as the product of O&M factors and energy produced in the former case, and as a sum of the wages of all citizens employed in the sector in the latter. Therefore, these two values may be different. The consideration of settlement cost eliminates this difference (details are given below). For a given company \(k\), \(x_{s,k}^t\) denotes a cost settlement in period \(t\), which gives the difference between the total O&M cost and the total labour cost for the entire power sector, in a given region, allocated based on the O&M cost of company \(k\), see Equation 37.

| $$\begin{split} \textrm{om}_j = \frac{y^t_j}{1-f_{\textrm{eloss},j}} f_{\textrm{om,j}}\\ x_{s,k}^t= \left(\sum_{j=1}^{J} \textrm{om}_j - \bar{w}^t l^t \right) \frac{\textrm{om}_k}{\sum_{j=1}^{J} \textrm{om}_j} \end{split}$$ | (37) |

Additionally, we define for each region the ratio of total labour cost in the electricity sector to total O&M cost, denoted \(r_{\textrm{om}}^t\), see Equation 38.

| $$r_{\textrm{om}}^t= \frac{\bar{w}^t l^t }{\sum_{j=1}^{J} \textrm{om}_j}$$ | (38) |

If the ratio \(r_{\textrm{om}}^t > 1\), the total labour cost in electricity sector is higher than the total O&M cost, and values of the factors \(f_{\textrm{om,j}}\) are adjusted for the next simulation step, in the manner defined in Equation 39, where the adjustment factor \(f_{\textrm{omadj}}\) is a simulation parameter. The factor \(f_{\textrm{om,j}}\) enables a smoother adjustment process.

| $$f_{\textrm{om,j}}^{t+1} = f_{\textrm{om,j}} \left(1 + f_{\textrm{omadj}} (r_{\textrm{om}}^t -1) \right)$$ | (39) |

Each power plant type is characterised by an overnight investment cost (USD/1kW). Additionally, for solar and wind energy we allow for a learning process that is modelled by a learning rate and the floor overnight investment cost. Thus for these plant types, the current overnight investment cost, \(\textrm{OIC}_\textrm{t}\), is defined in Equation 40 (as in the MIND model (Edenhofer et al. 2005)).

| $$\textrm{OIC}_\textrm{t} = \textrm{OIC}_\textrm{floor} + (\textrm{OIC}_\textrm{initial} - \textrm{OIC}_\textrm{floor}) \times \left(\frac{\textrm{TIC}_\textrm{t}}{\textrm{TIC}_\textrm{initial}}\right)^\textrm{lr}$$ | (40) |

\(\textrm{OIC}_\textrm{floor}\) represents the floor overnight investment cost, \(\textrm{TIC}\) stands for the total installed capacity of solar or wind. Variable \(\textrm{lr}\) represents the learning rate, as it is assumed that for new technologies (solar and wind) that the more units produced the more efficient the production becomes, \(\textrm{lr}<0\). For the storage capacity, we use a simplified version, see Equation 41. Furthermore, electricity storage technology (e.g. batteries) develops independently from the storage capacity actually installed and operating in electricity grids. This is due to, for example, the rapid development of electric cars. The value of the parameter \(\textrm{lr}\) is set to \(0.99\).

| $$\textrm{OIC}_\textrm{t} = \textrm{OIC}_\textrm{floor} + (\textrm{OIC}_\textrm{t-1} - \textrm{OIC}_\textrm{floor}) \times \textrm{lr}$$ | (41) |

To be able to take into account both changing capital goods prices and changing overnight investment cost, we model physical capital as the product of capacity and the overnight investment cost, whereas capital value remains a product of physical capital and the capital goods price (actual capital expenditures). The total capital value \(\textrm{kv}^t\) and total capacity \(c_p^t\) are allocated to individual years over the power plant lifetime \(T\), see Equation 42, with \(i=1\) the oldest and \(i=T\) the newest part.

| $$\begin{split} \textrm{kv}^t=\sum_{i=1}^{T} \textrm{kv}_i^t \\ c_p^t=\sum_{i=1}^{T} c_{p,i}^t \\ \end{split}$$ | (42) |

At the end of the simulation period \(t\), capital is depreciated by liquidating the oldest part of capacity, according to the formula in Equation 43[6].

| $$\begin{split} \textrm{kv}_d^t = \textrm{kv}^t - \textrm{kv}_1^t \\ c_{pd}^t = c_p^t - c_{p,1}^t \\ \end{split}$$ | (43) |

Additionally, for solar and wind power plants a storage capacity $c_s^t$ is depreciated in a simplified standard way, Equation 44.

| $$c_{sd}^t = c_{s}^t * (1-f_{\textrm{depr}})$$ | (44) |

The planned electricity price for period \(t+1\) is set to the marginal production cost, which consists of the O&M cost in period \(t\) and the fuel price in period \(t\) (a power plant does not forecast changes in fuel prices), if relevant for the power plant type, and is given by Equation 45.

| $$\widetilde{p}^{t+1}_j = \frac{f_{\textrm{om,j}}^{t+1} + \frac{p_f^t}{f_\textrm{conveff}} (1-f_{\textrm{sub}})}{1-f_{\textrm{eloss},j}}$$ | (45) |

The planned electricity available over a given time period \(\widetilde{y}^{t+1}_j\) is calculated in different ways for different power plant types. For nuclear power plants, which are characterised by a stable operation mode, we use the deterministic approach and calculate the planned electricity produced as the product of installed capacity and the capacity availability factor, see Equation 46.

| $$\begin{split} \widetilde{y}^{t+1}_j = c_{p,j}^t f_{\textrm{capacity}} (1-f_{\textrm{eloss},j}) \Delta t \end{split}$$ | (46) |

For all the other types of power plants, the energy available in the current period is modelled with a beta distribution (Gupta & Nadarajah 2004) with parameters \(\alpha\) and \(\beta\). This expresses the fact that for solar and wind energy power plants the actual energy produced is stochastic and depends on the weather conditions, whereas for other power plant types the stochasticity is related to necessary downtime related to maintenance. The parameter values are given in Equation 47. The parameters are set in such a way that the mean availability equals the capacity factor — \(f_{\textrm{capacity}}\).

| $$\begin{split} \alpha = 2 \\ \beta = \alpha \times \frac{1 - f_{\textrm{capacity}}}{ f_{\textrm{capacity}}} \\ \end{split}$$ | (47) |

Then for all other types of power plants, with the exception of solar power plants, electricity available in a given time period \(\widetilde{y}^{t+1}_j\) is then calculated according to Equation 48. \(F^{-1}_{\alpha,\beta}\) is an inverse cumulative probability distribution function having a Beta distribution with the parameters \(\alpha\) and \(\beta\), and \(\nu\) is a uniformly distributed random variable.

| $$\begin{split} \widetilde{y}^{t+1}_j = c_{p,j}^t F^{-1}_{\alpha,\beta}(\nu) (1-f_{\textrm{eloss},j}) \Delta t \end{split}$$ | (48) |

For solar power plants, electricity available in a given time period \(\widetilde{y}^{t+1}_j\) is calculated according to Equation 49, in order to take into account the fact that solar energy is only available during daylight.

| $$\begin{split} \textrm{day}: \widetilde{y}^{t+1}_j = 2 c_{p,j}^t F^{-1}_{\alpha,\beta}(\nu) (1-f_{\textrm{eloss},j}) \Delta t \\ \textrm{night}: \widetilde{y}^{t+1}_j = 0 \\ \end{split}$$ | (49) |

Additionally, for solar and wind energy power plants the amount of available energy is increased by the amount of stored energy multiplied by \((1-f_{\textrm{eloss},j})\). The maximum electricity available in a given time period is calculated according to Equation 50 for coal, gas, oil, and nuclear power plants, thus allowing for an additional capacity reserve, calculated using the reserve rate \(r_{\textrm{spin}}\).

| $$\begin{split} \widetilde{y}^{t+1}_{\textrm{max},j} = \widetilde{y}^{t+1}_j (1+r_{\textrm{spin}}) \end{split}$$ | (50) |

In each period a certain share of capacity, which is as old as the power plant lifetime[7], is replaced with planned investments. The decision depends on whether the power plant capacity after depreciation would be able (on average) to cover the maximum demand in the next simulation step. For the condition to be verified (Equation 51), the following parameters need to be taken into account for this decision: the required capacity reserve (\(r_{\textrm{cap}}\)), the spinning reserve for fuels power plants (\(r_{\textrm{spin}}\)), and a time slice (\(\Delta t\)).

| $$c_{pd}^t (1-f_{\textrm{eloss}}) \times \Delta t \times f_{\textrm{capacity}} > y^t_{\textrm{max}} (1+f^1_{\textrm{gdp}}) (1 + r_{\textrm{cap}}) (1+r_{\textrm{spin}})$$ | (51) |

Let us assume that the condition, given in Equation 51 is satisfied. In this case, the total installed capacity will be gradually decreased. The planned partial replacement \(\Delta c_{p}^t\) is given by Equation 52, where \(e_{\textrm{down}}\) and \(e_{\textrm{freeze}}\) are simulation parameters, and \(\nu\) is a uniformly distributed random variable.

| $$c_{pd}^t (1-f_{\textrm{eloss}}) \times \Delta t \times f_{\textrm{capacity}} > y^t_{\textrm{max}} (1+f^1_{\textrm{gdp}}) (1 + r_{\textrm{cap}}) (1+r_{\textrm{spin}})$$ | (52) |

The parameter \(e_{\textrm{freeze}}\) is calculated according to Equation 53, based on the simulation parameter values \(\textrm{red}\) and \(\textrm{period}\).

| $$e_{\textrm{freeze}} = e_{\textrm{red}}^{\lfloor{\frac{\textrm{step}}{\textrm{period}}}\rfloor}$$ | (53) |

This limits the magnitude of the changes in the electricity market structure occurring over a fixed number of periods (denoted by \(\textrm{period}\)) by using the reduction rate value \(e_{\textrm{red}}\) (without this factor, one would obtain geometric growth rates of capacities and potential overinvestment in later simulation steps). Let us now assume that the condition given in Equation 51 is not satisfied.In this case, the total installed capacity will be gradually increased, and the planned replacement \(\Delta c_{p}^t\) is calculated according to Equation 54.

| $$\left(c_{p}^t-c_{pd}^t \right) \left(1 + \textrm{max}(1,e_{\textrm{up}} e_{\textrm{freeze}}) f_{\textrm{prod}} \nu\right)$$ | (54) |

\(e_{\textrm{up}}^{\textrm{w}}\), nuclear and hydro \(e_{\textrm{up}}^{\textrm{nh}}\). This allows us to capture differences in constraints for different power plants (e.g. natural, as in the case of hydro, or political, as in case of nuclear). In the case of the following regions (Africa, Commonwealth of Independent States, and Middle East), the initial wind and solar power plant capacities are negligibly low, so for these regions the replacement rate for wind and solar power plants is defined by a constant \(e_{\textrm{up}}^{\textrm{af}}\). Finally, total planned capacity is adjusted by the planned GDP growth rate for the second consecutive period, see Equation 55.

| $$\widetilde{c}_{p}^{t+1} = \left(c_{p}^t+ \Delta c_{p}^t \right)(1+f^1_{\textrm{gdp}})$$ | (55) |

Additionally, solar and wind energy companies may also invest in storage capacity (apart from investments in power capacity). We assume that a company will invest in storage capacity if storing the energy is more profitable than additional potential energy production. This means that instead of selling the energy to the market when electricity prices are relatively low, the solar (wind) power plant could store the energy and sell it when electricity prices are relatively high. We capture this idea by assuming that the company invests in storage capacity based on the distribution of historical market electricity prices. This applies when the ratio of the interquartile range of electricity prices to the current overnight investment cost of storage capacity is higher than twice the ratio of the average electricity price to the current overnight investment cost of power capacity, see Equation 56. We assumed that energy can be stored in one period and used in the subsequent period.

| $$\frac{2\bar{p}^t}{\textrm{OIC}_p} < \frac{p^t_{\textrm{Q3}}-p^t_{\textrm{Q1}}} {\textrm{OIC}_s}$$ | (56) |

The total planned storage capacity is then calculated according to Equation 57.

| $$\widetilde{c}_s^{t+1} = max\left(c_s^t (1+f_{\textrm{prod}}\nu), \frac{c_p^t}{T}\right)\left(1+f^1_{\textrm{gdp}}\right)$$ | (57) |

Otherwise, it is calculated according to Equation 58.

| $$\widetilde{c}_s^{t+1} = \left(c_s^t (1-f_{\textrm{prod}}\nu)\right)\left(1+f^1_{\textrm{gdp}}\right)$$ | (58) |

The power plant plans the required fuel stocks for the next period \(t+1\) in a simplified way. The planned amount is, based on the previous period production, forecasted GDP growth rate and necessary stock rate \(r_{\textrm{cap}}\), see Equation 59. \(s_f^t\) are the stocks left from the previous period.

| $$\widetilde{s}_f^{t+1} = \textrm{max}\left(\frac{y^t}{f_{\textrm{conveff}}}(1 + r_{\textrm{cap}}) (1+f_{\textrm{gdp}}),s_f^t\right)$$ | (59) |

For fuel-fired (coal, gas, oil) power plants, we also take into consideration limitations due to the fuel stocks currently available for electricity production in a given simulation step.

Market Clearing Mechanisms

This section provides a detailed discussion of market clearing mechanisms, which are examined in the following order:

- Capital markets

- Labour markets

- Fuel markets

- Electricity markets

- Capital goods markets

- Consumer goods markets

Capital markets

As mentioned earlier, a capital market is demand driven and is modelled in a simplified way. Let us consider a simulation period \(t+1\) and a given region. We consider all \(I\) citizens living in this region, indexed by \(i\), and all \(J\) companies from this region, indexed by \(j\). First, the capital raised by company \(j\) is calculated as the sum of new capital that is planned for investment in company \(j\) in the next period \(t+1\) by citizens (denoted \(\widetilde{o}^{t+1}_{i,j}\) for citizen i, see also Equation 19, see Equation 60.

| $$\widehat{\Delta \textrm{kv}}^{t+1}_j = \sum_{i=1}^{I} \widetilde{o}^{t+1}_{i,j}$$ | (60) |

Second, citizens' shares in companies are updated. According to Equation 61, the new capital ratio \(r^{t+1}_{\textrm{ni},j}\) is calculated, where \(\textrm{kv}^t_j\) is the current capital value and \(s^t_j\) the current cash at hand value.

| $$r^{t+1}_{\textrm{n},j} = min\left(\frac{\widehat{\Delta \textrm{kv}}^{t+1}_j}{\widehat{\Delta \textrm{kv}}^{t+1}_j +\textrm{kv}^t_j + s^t_j},1\right)$$ | (61) |

Then, citizens’ shares in a company (\(h_{i,j}^{t+1}\) denotes a capital share of a citizen \(i\) in a company \(j\) in a simulation period \(t\)) are updated as a weighted mean of new capital and existing capital owned by company \(j\), as presented in Equation 62.

| $$h_{i,j}^{t+1} = r^{t+1}_{\textrm{n},j} \frac{\widetilde{o}^{t+1}_{i,j}}{\widehat{\Delta \textrm{kv}}^{t+1}_j} + (1-r^{t+1}_{\textrm{n},j}) h_{i,j}^{t}$$ | (62) |

The planned capital value increase in period \(t+1\), denoted as \(\widetilde{\Delta \textrm{kv}}^{t+1}_j\) is limited from above by the value of the capital raised \(\widehat{\Delta \textrm{kv}}^{t+1}_j\). \(\widetilde{\Delta \textrm{kv}}^{t+1}_j\) is calculated for a company as the difference between planned physical capital, necessary for production in the period \(t+1\), and the available physical capital at the beginning of simulation period \(t+1\), multiplied by the expected price of the production goods. The difference between collected capital \(\widehat{\Delta \textrm{kv}}^{t+1}_j\) and the increase in actual total capital in period \(t+1\) is subsequently distributed among owners in proportion to the number of shares held in a given company.

Labour markets

The labour market is also modelled in a simplified way. Private households looking for a job are randomly matched with companies looking for employees. In a more detailed way. First, a company for which the current labour in step \(t\) exceeds the planned labour for step \(t+1\) by at least one employee \(k^t-\widetilde{k}^{t+1}\ge1\) and having at least one employee \(k^t>1\) lays off unnecessary employees. Second, only the companies for which the planned labour[8] for step \(t+1\) exceeds the current labour[9] in step \(t\) by at least half \(\widetilde{k}^{t+1}- k^t\ge 0.5\) are considered as looking for employees. Third, unemployed citizens are randomly matched with companies looking for employees in a stepwise manner. At each single step. one unemployed citizen and one company looking for employees are selected and matched. A citizen will receive the average wage at the company. If \(\widetilde{k}^{t+1}- k^t< 0.5\), a company is no longer interested in looking for employees. The process stops if there are either no more companies looking for employees or no more unemployed citizens. In the final step, regional unemployment rates \(r_{\textrm{unemp}}^{t+1}\) are calculated and then unemployment factors, as given in Equation 63. \(s_{\textrm{unemp}}\) is a simulation parameter.

| $$f_{\textrm{unemp}}^{t+1} = 1 - \textrm{min}\left(1, \frac{r_{\textrm{unemp}}^{t+1}}{s_{\textrm{unemp}}}\right)$$ | (63) |

Moreover, as discussed earlier, since the number of power plants reflects technical considerations and not the number of citizens employed in this sector, the number of power plants is much higher than the number of employed citizens. Therefore, citizens are not directly assigned to a power plant but the labour cost is proportionally (to production) distributed among power plants. The number of electricity sector employees is kept constant during the simulation for simplicity.

Fuel markets

Fuel markets are modelled as centrally cleared markets, separately for each type of fuel \(f\): coal, crude oil and gas. The \(J\) fuel extraction companies offer the fuel at their marginal extraction cost with regular and maximum quantities. The \(I\) fuel consuming agents (citizens, consumer goods and capital goods companies, power plants) bid the quantities and accept the market price (we assume that the demand for fuels is inelastic in the short term). Total fuel demand is calculated as the sum of individual planned consumption for the fuel consuming agents (citizens as a result of utility, and consumer/capital goods companies as a result of profit maximisation) according to Equation 64. Additionally, planned fuel demand for power plants is calculated as the difference between planned fuel stocks and current fuel stocks, see Equation 65.

| $$d_f^{t+1} = \sum_{i=1}^{I} \widetilde{x}_{f,i}^{t+1}$$ | (64) |

| $$\widetilde{x}_{f,i}^{t+1} = \widetilde{s}_{f,i}^{t+1} - {s}_{f,i}^{t}$$ | (65) |

Total fuel supply is calculated as the sum of planned production (fuel extraction) of all fuel extraction companies, according to Equation 66.

| $$s_f^{t+1} = \sum_{j=1}^{J} \widetilde{y}_{f,j}^{t+1}$$ | (66) |

Total maximum fuel supply is calculated analogously by summing the planned maximum production, according to Equation 67.

| $$s_{f,max}^{t+1} = \sum_{j=1}^{J} \widetilde{y}_{f,max,j}^{t+1}$$ | (67) |

In the next step, total demand is compared with both total supply and total maximum fuel supply. We consider three separate cases. In the first case, total demand is lower or equal to the total supply; in the second case, total demand is higher than total supply but lower or equal to the maximum supply; and in the third case, total demand is higher than maximum supply.

- \(d_f^{t+1} \le s_f^{t+1}\)

- \(s_f^{t+1} < d_f^{t+1} \le s_{f,max}^{t+1}\)

- \(d_f^{t+1} > s_{f,max}^{t+1}\)

We also order the suppliers according to the offer price (marginal extraction cost), from lowest to highest, then calculate the market price \(p_f^{t+1}\) and clear transactions.

In the first of the three cases considered, the market price is calculated as the intersection point of the demand and supply curves, see Equation 68 for calculation details.

| $$\begin{split} k: \sum_{j=1}^{k-1} \widetilde{y}_{f,j}^{t+1} < d_f^{t+1} \wedge \sum_{j=1}^{k} \widetilde{y}_{f,j}^{t+1} \ge d_f^{t+1} \\ p_f^{t+1} = \widetilde{p}_{f,k}^{t+1} \\ \end{split}$$ | (68) |

Then for each fuel consuming agent, current demand in step \(t + 1\) is set to the value of planned demand \(x_{f,i}^{t+1} = \widetilde{x}_{f,i}^{t+1}\). For all producers whose planned price is lower than the market price, current production equals planned production \(y_{f,j}^{t+1} = \widetilde{y}_{f,j}^{t+1}\). For all producers with planned price equal to the market price, current production equals planned production multiplied by the factor (assures proportional reduction) defined in Equation 69, where \(k_\textrm{min} = \textrm{min}(j: \widetilde{p}_{f,j}^{t+1} = p_f^{t+1})\) and \(k_\textrm{max} = \textrm{max}(j: \widetilde{p}_{f,j}^{t+1} = p_f^{t+1})\).

| $$f_{\textrm{supply1}} = \frac{d_f^{t+1} -\sum_{j=1}^{k_{\textrm{min}}-1} \widetilde{y}_{f,j}^{t+1} }{\sum_{j=k_{\textrm{min}}}^{k_{\textrm{max}}} \widetilde{y}_{f,j}^{t+1}}$$ | (69) |

For producers having a planned price higher than the market price, the current production equals \(0\).

In the second case, the market price equals the planned price of the producer having the highest planned price. Additionally, it might have been increased by multiplication with the first stress factor \(f_\textrm{fuelStress1}\), see Equation 70. However, we set the values of both fuel stress factors: \(f_\textrm{fuelStress1}\) and \(f_\textrm{fuelStress2}\) (introduced later) to 1, in order to have exactly the same fuel price dynamics as given by the Rogner curve.

| $$p_f^{t+1} = \widetilde{p}_{f,J}^{t+1} \times f_\textrm{fuelStress1}\\$$ | (70) |

Then for each fuel consuming agent, current demand in step \(t + 1\) equals planned demand \(x_{f,i}^{t+1} = \widetilde{x}_{f,i}^{t+1}\). The excess demand is distributed among producers proportionally, see Equation 71.

| $$\begin{split} f_{\textrm{supply2}} = \frac{d_f^{t+1}-s_{f}^{t+1}}{s_{f,max}^{t+1}-s_{f}^{t+1}} \\ y_{f,j}^{t+1} = \widetilde{y}_{f,j}^{t+1} + f_{\textrm{supply2}} \left(\widetilde{y}_{f,max,j}^{t+1} - \widetilde{y}_{f,j}^{t+1}\right) \\ \end{split}$$ | (71) |

Finally, in the third case, the market price equals the planned price of the producer having the highest planned price. It might have been additionally increased by multiplication with the second stress factor \(f_\textrm{fuelStress2}\), see Equation 72.

| $$p_f^{t+1} = \widetilde{p}_{f,J}^{t+1} \times f_\textrm{fuelStress2}\\$$ | (72) |

Then for each fuel consuming agent, current demand in step \(t + 1\) equals planned demand reduced proportionally, see Equation 73.

| $$\begin{split} f_{\textrm{demand3}} = \frac{s_{f,max}^{t+1}}{d_f^{t+1}} \\ x_{f,i}^{t+1} = \widetilde{x}_{f,i}^{t+1} \times f_{\textrm{demand3}} \\ \end{split}$$ | (73) |

For each fuel producer, current production in step \(t + 1\) equals maximum production \({y}_{f,j}^{t+1} = \widetilde{y}_{f,max,j}^{t+1}\). For all the three cases considered above, and for each fuel extraction company, the current demand is set to the value of current production \(y_{f,j}^{t+1}\) = \(y_{f,j}^{t+1}\). As a result, a fuel extraction company will try to increase fuel extraction (in line with forecast GDP growth) by increasing the amount of physical capital if the actual production was higher than planned production, and will decrease production otherwise, as described in Equation 30.

Electricity markets

Electricity markets function in a similar way to the fuel markets, but only on the regional level and not on a global level as is the case for fuel markets. Moreover, we consider \(N_e\) different electricity market clearing periods in a single simulation step. In this way, we can take into account randomness in power generation, since power output from wind and solar installations may be different in each of the clearing periods. To model the periodicity of the electricity demand, we have introduced alternately changing periods of high and low electricity demand (we model the day and night demand regimes with peaks in daytime and lows at nighttime). We do not model the seasonality for reasons of simplicity. However, it must be mentioned that demand partially levels off at the regional level (compared to the national level or the even finer levels observed in practice) and the increased winter electricity demand (for heating purposes) may be balanced to some extent by the increased summer demand for cooling purposes. Total electricity demand is calculated as the sum of individual demand, according to Equation 74.

| $$d_e^{t+1} = \sum_{i=1}^{I} \widetilde{x}_{e,i}^{t+1}$$ | (74) |

Total electricity supply is calculated as the sum of individual electricity that can be supplied by the power plants, according to Equation 75.

| $$s_e^{t+1} = \sum_{j=1}^{J} \widetilde{y}_{e,j}^{t+1}$$ | (75) |

Total maximum electricity supply is calculated analogously by summing the maximum amount of electricity that can be supplied by power plants, according to Equation 76.

| $$s_{e,max}^{t+1} = \sum_{j=1}^{J} \widetilde{y}_{e,max,j}^{t+1}$$ | (76) |

Next, total demand is compared with total supply and total maximum electricity supply. We consider three cases. In the first case, total demand is lower or equal to total supply; in the second case, total demand is higher than total supply but lower or equal to the maximum supply; in the third case, total demand is higher than maximum supply:

- \(d_e^{t+1} \le s_e^{t+1}\)

- \(s_e^{t+1} < d_e^{t+1} \le s_{e,max}^{t+1}\)

- \(d_e^{t+1} > s_{e,max}^{t+1}\)

The subsequent steps and calculations are almost identical to the case of fuel markets. We consider different values of stress factors in the case of electricity markets (price increases are observed in case of the market stress), however.

Initially, we observed a relatively low share of electricity produced by peak load power plants (gas and oil fired) in the simulation results, when compared to the empirical data. This might be caused by the aggregation of the many national electricity markets into one market for each region (diversification of electricity production may reduce the need for expensive peak load sources). Such aggregation is limited in reality, not only due to administrative reasons (borders or separate grids for countries) but also due to network constraints (limited capacity of the power grid). In order to also take this mechanism into account, a certain percentage of coal power plant electricity production is replaced with gas and crude oil power plant electricity production (the coal power percentage being calibrated so that the simulated and empirical energy mix agree for each region in the first initial simulation step). The introduced constraint is relaxed with each simulation step (by multiplying the electricity production to be shifted to the peak power plant by a constant equal to 99%, to allow for gradual relaxation of the introduced network constraint; this may represent a gradual extension of the electricity network). In particular, the amount of additionally produced electricity by oil power plants \(\Delta_{e,\textrm{oil}}^{t+1}\) is shown in Equation 77. \(f_{\textrm{min,oil}}\) is a simulation factor (giving the percentage of electricity supply to be satisfied by oil power plants during peak load), \(s_{e,\textrm{oil}}^{t+1}\) is the unconstrained electricity supply by oil power plants.

| $$\Delta_{e,\textrm{oil}}^{t+1} = \textrm{max}\left(f_{\textrm{min,oil}} \times s_e^{t+1}- s_{e,\textrm{oil}}^{t+1},0\right)$$ | (77) |

The amount of additionally produced electricity by oil power plants \(\Delta_{e,\textrm{gas}}^{t+1}\) is calculated in an analogous way. Both values can be scaled down by the factor defined in Equation 78, which takes into consideration the actual supply by coal power plants (the electricity generation increase of oil and gas power plants is limited by the potential decrease of such generation by coal power plants).

| $$\textrm{min}\left(\frac{s_{e,\textrm{coal}}^{t+1}}{\Delta_{e,\textrm{oil}}^{t+1} + \Delta_{e,\textrm{gas}}^{t+1}},1\right) $$ | (78) |

The market clearing price is also finally recalculated as a weighted mean and adjusted in the manner defined in Equation 79. It is assumed that all electricity consumers cover the cost of the network constraints.

| $$p_e^{t+1} = \frac{d_e^{t+1} - \Delta_{e,\textrm{oil}}^{t+1} - \Delta_{e,\textrm{gas}}^{t+1}}{d_e^{t+1}} \times p_e^{t+1} + \frac{\Delta_{e,\textrm{gas}}^{t+1}}{d_e^{t+1}} \times \textrm{max}(p_e^{t+1}, \widetilde{p}_{\textrm{gas}}^{t+1}) + \frac{\Delta_{e,\textrm{oil}}^{t+1}}{d_e^{t+1}} \times \textrm{max}(p_e^{t+1}, \widetilde{p}_{\textrm{oil}}^{t+1}) $$ | (79) |

For the Middle East, electricity produced by gas power plants may be shifted to electricity produced by oil power plants in an analogous way. If the electricity storage capacity is available, produced but unconsumed electricity is stored.

Capital goods market

The capital goods market is a global market but with local interactions. The demand side of the market consists of fuel extraction, electricity, capital goods companies and consumer goods companies. The demand for capital goods for company \(i\) equals the minimum of the planned physical capital increase, \(\widetilde{\Delta k}_i^{t+1}\), and the planned monetary value of the capital increase \(\widetilde{\Delta kv}_i^{t+1}\), divided by the capital goods price. In this way, a capital goods price increase may lower the demand for these goods. The supply side consists of capital goods companies, with the supply for company \(j\) being \(y_j^{j+1}\). The market is modelled in a simplified way. Namely, we allow for capital goods companies to produce the necessary capital increase for their own use beforehand. Furthermore, this part of capital is also available from the beginning of the simulation step.

We know that, in the general case, the increase in planned physical capital — and consequently its value — is bounded by the equation — \(\widetilde{\Delta \textrm{kv}}_j^{t+1} = \widetilde{\Delta \textrm{k}}_j^{t+1} \times \bar{p}_{pg}^t\). In the case of the power plants, the planned physical capital increase is calculated as the product of the planned capacity increase \(\widetilde{\Delta c_p}_j^{t+1}\) and the current value of the overnight investment cost \(\textrm{OIC}_\textrm{t+1}\), according to the formula specified in Equation 80. As a result, we can model decreasing OIC due to increased efficiency for different types of power plants.

| $$\widetilde{\Delta \textrm{k}}_j^{t+1} = \widetilde{\Delta c_p}_j^{t+1} \times \textrm{OIC}_\textrm{t+1}$$ | (80) |

For solar and wind power plants, acquired capital goods are divided between electricity production and storage capacities, based on the proportion of existing capacities.

To model the local market — market fragmentation — we implement an adaptive approach with local interactions (Assenza et al. 2015). Each customer is connected to a certain number of producers (companies). A customer first buys from the connected producer that offers the lowest price. When the total demand exceeds the total supply of a company, the demand is only partly satisfied (in the same proportion for each customer). A customer with unsatisfied demand turns to the next connected company with the second lowest price, and so on.